NOTE: Betterment is offering up to 1 year free to new users. Find out full details here. Read our updated Betterment review here.

Lately I’ve been hearing a lot about a new investing website and brokerage account through Betterment.com. What is Betterment? At its very basic it’s another in a long line of online brokerages that allow you to hold stocks and bonds as investments via ETFs, like an account through Etrade or Ally Invest.

But it’s more than just that. It’s also a tool that helps automate the investing process to make it simpler for the average user, and for those who are just too busy to stay on top of their investing accounts all of the time. So today I thought I’d do a review of Betterment.com.

Quick Navigation

Betterment Background

Betterment.com was founded by Jon Stein in 2008. Betterment.com launched at TechCrunch Disrupt 2010 NYC. In December 2010 Betterment.com received $3 Million in a Series A financing round from Bessemer Venture Partners (lead) and Anthemis Group.

Betterment LLC is a Registered Investment Advisor with the SEC and they’re SIPC insured. You can be assured of the same protections as you would with a larger financial institution. Of course, since this is an investing account and not a savings account, there is no assurance of not losing your money.

Betterment launched in 2010, and in only a short time after their launch, they were receiving a lot of buzz with writeups in The New York Times, CNNMoney, Investment News, Mint.com, and more.

Awards

When the website launched at the end of 2010, it was already receiving quite a bit of recognition for its innovative ideas and approach.

- TechCrunch Disrupt NYC 2010 “Battlefield Finalist”

- TechCrunch Disrupt NYC 2010 “Best NYC Startup”

- FinovateFall 2010 “Best of Show”

- 2014 – The First Automated Investing Service to Reach 50,000 Customers With More Than $1 Billion Under Management.

- 2015 – The First Automated Investing Service to Reach 75,000 Customers With More Than $1.7 Billion Under Management.

- 2015 – Added to the FT300, the Financial Times’ list of Top Financial Advisors.

- 2016 – Wealth Management Award Winner for best 401(k) Retirement Plan Support Services.

- 2017 – Benzinga Fintech Award Winners for best robo-advisor.

- 2019 – Investopedia Best Robo-Advisor

- 2020 – Investopedia – Best for CashManagement

Since they launched over a decade ago they’ve had plenty of recognition for their innovated investing tools, and now have over 500,000 happy customers and over $22 Billion in assets under management! Not too shabby.

How Does Betterment Work?

So what exactly is Betterment, and how does it work? The basic idea is this – a lot of people are either just too busy to get too far into the weeds with their investment decisions, or they are too intimidated by the array of choices out there when it comes to investing. Betterment attempts to take the confusion out of the process by making investing simple.

So when you set up an investment account with Betterment, they make the process super simple. After you signup, The only choices you’ll need to make are:

- How much to invest.

- How much of your investment you want in equities (Stock Market).

- How much you want in bonds.

You can also set up automatic investments on a regular basis if you want to.

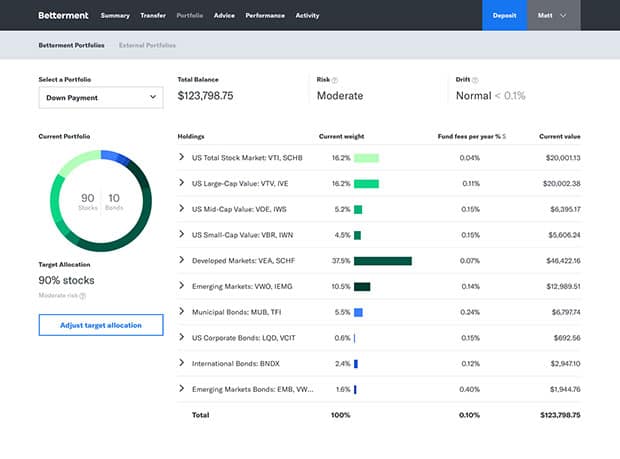

Within stocks and bonds, they divide up your holdings into a variety of ETFs so that you are diversified. Here is what you get on the stocks side:

- Vanguard Total Stock Market ETF (VTI)

- Vanguard US Large-Cap Value Index ETF (VTV)

- Vanguard US Mid-Cap Value Index ETF (VOE)

- Vanguard US Small-Cap Value Index ETF (VBR)

- Vanguard FTSE Developed Market Index ETF (VEA)

- Vanguard FTSE Emerging Index ETF (VWO)

For bond ETFs here is what you get:

- iShares Short-Term Treasury Bond Index ETF (SHV)

- Vanguard Short-term Inflation-Protected Treasury Bond Index ETF (VTIP)

- Vanguard US Total Bond Market Index ETF (BND)

- iShares National AMT-Free Muni Bond Index ETF (MUB)

- iShares Corporate Bond Index ETF (LQD)

- Vanguard Total International Bond Index ETF (BNDX)

- iShares J.P. Morgan USD Emerging Markets Bond ETF (EMB)

The exact allocations of each stock or bond ETF will depend on the allocation you choose. Either way, the stocks and bonds you get will give you a nice diversified portfolio.

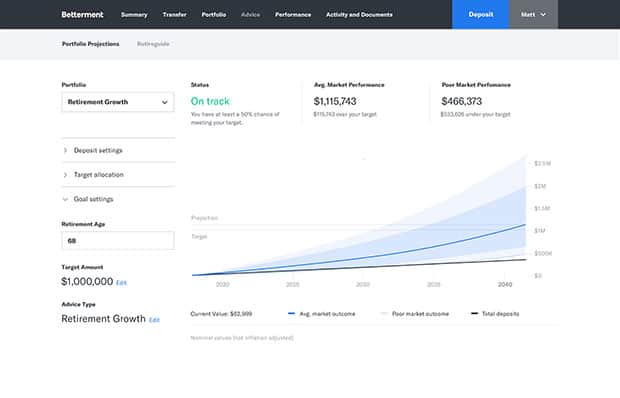

Asset Allocation And Visualization Tools

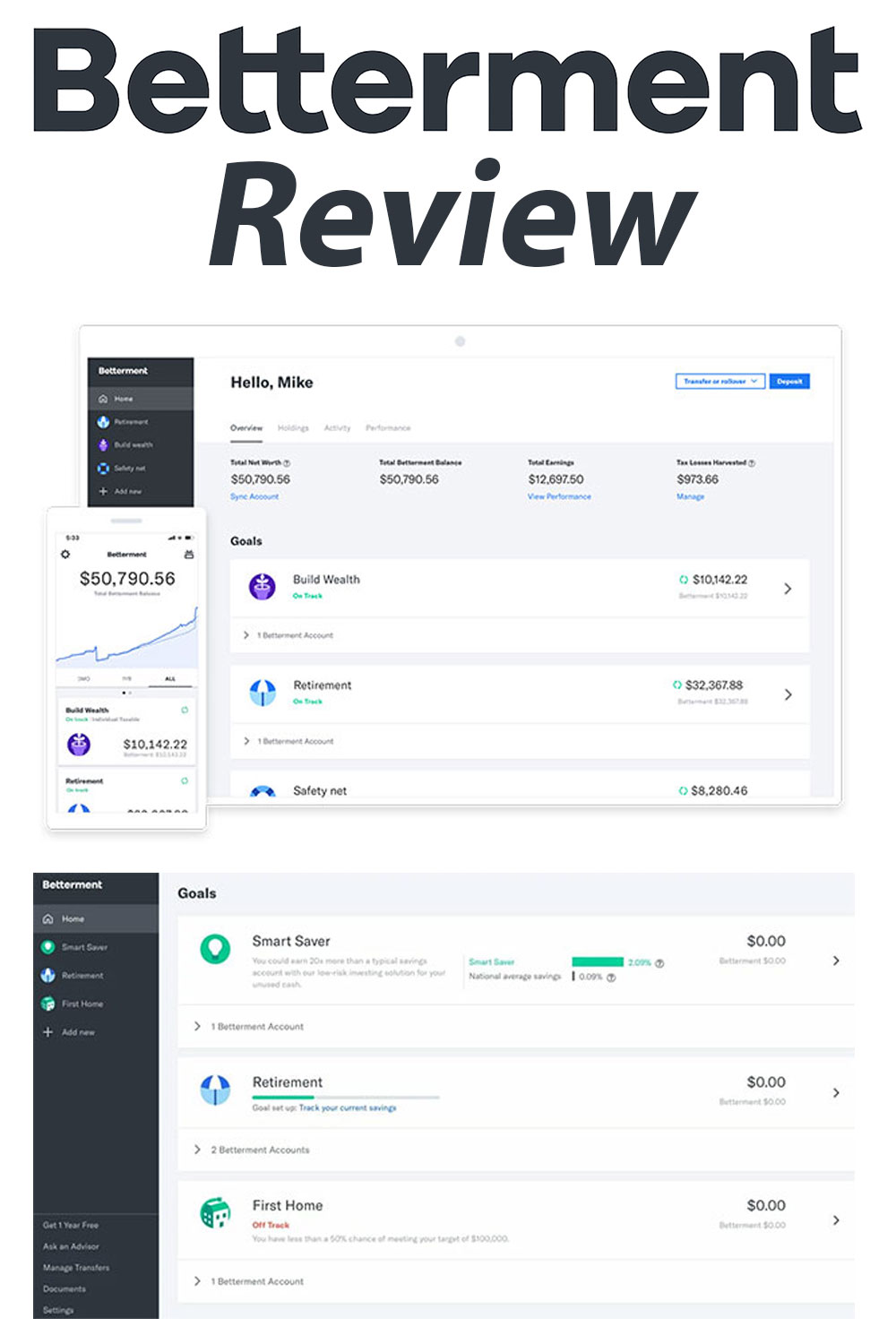

To me one of the selling points of Betterment is the allocation and visualization tools you can use to set your investment goals. You can update your asset allocation, and investing time horizon and see what kind of returns you can expect to see given your amount invested, level of risk, and historical returns. It’s pretty interesting to play with the tool and see the differences you can expect given different allocations.

Let’s say that you have about $50,000 invested as the demo account does. If you have 80% invested in stocks and 20% in bonds, given a 20-year time horizon it will show you a forecasted range of returns that you could expect to see – anywhere from $100,000-$600,000. Change the percentages and timelines and it can drastically affect your results.

So if you decide you want to change your allocation either to include more stocks or bonds, you just move the slider up or down and then hit the “change” button, and Betterment will update your account holdings and purchasing decisions going forward. Piece of cake!

Automatic Re-allocation

One of the nice things about an account with Betterment is that it will automatically re-balance your portfolio for you every three months, or if your allocations drift more than 5%. Without re-balancing, your account can easily shift over time to have an allocation that is heavier on stocks or bonds than you want it to be. If you start out at say 80/20 stocks to bonds, if you don’t reallocate over time you could one day find that your account has an allocation more like 75/25 or 70/30.

This is one of those things that most investors neglect to do on a regular basis, so it’s nice to have that part of the account be automatic.

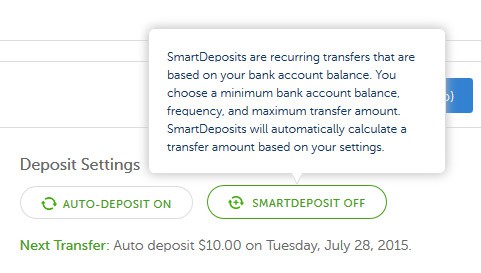

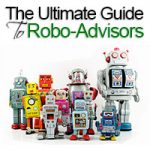

SmartDeposit

Betterment has a feature called SmartDeposit. What is it? SmartDeposit is a way to ensure that you’re investing more money in the stock market via Betterment instead of just letting it sit in your checking account. How does it work?

You go into your Betterment account and turn on the SmartDeposit feature for your taxable investing account (it isn’t available for IRAs currently). Once you enable it it will ask you want the maximum amount you need in your bank account is, and how much Betterment should invest at a time.

Once Betterment has that information it will automatically invest any excess cash in your checking account over the amount you set. Betterment will check your account at least once a week.

You’ll receive notifications of any pending transfers so you can modify or cancel the transaction for up to 24 hours before it happens.

Tax Efficient Investing

One big change that Betterment has made in the past couple of years was to implement a more tax-efficient philosophy. They have implemented strategies to make Betterment more tax-efficient and increase returns for most users.

Tax Loss Harvesting

Betterment will look at your portfolio and help offset your capital gains through Tax Loss Harvesting – which could add an estimated +0.77% in after-tax returns, annually. So what exactly is Tax Loss Harvesting?

Tax loss harvesting is the practice of selling a security that has experienced a loss. By realizing, or “harvesting” a loss, investors are able to offset taxes on both gains and income. The sold security is replaced by a similar one, maintaining the optimal asset allocation and expected returns

While tax-loss harvesting used to have a $50,000 account balance minimum, it is now included at no cost for all users!

TaxMin Lot Selling

Betterment helps save on taxes by using TaxMin Lot Selling.

Choosing which lots of shares to sell can greatly impact the investment taxes you pay. Using our TaxMin cost basis accounting method, we go beyond the industry standard (FIFO). We intelligently liquidate each of your lots when you withdraw to minimize your capital gains.

Tax Impact Preview

Betterment will give you real-time tax information that will help you to make more informed investing decisions. If you decide to change your allocation or make a withdrawal, their Tax Impact Preview tool will allow you to see what kind of an impact the change will have on your taxes, and returns.

Tax-Efficient Investments

Betterment only invests in exchange-traded funds (ETFs) which are generally more tax-efficient, when compared to mutual funds. Investing in ETFs can provide an estimated .7% in tax savings per year.

Smart Rebalancing

Betterment uses cash flow and dividend reinvestment in order to reduce the need to sell shares to rebalance your account. This can lower your capital gains taxes over time.

Betterment Cash Reserve And Checking Accounts

Up until July of 2019 Betterment had an alternative to the high-yield savings products offered by online banks called Betterment Smart Saver. Your money was invested in very short-term securities that pay comparable rates to those offered on online savings accounts and CDs.

Betterment announced the release of their new Betterment Cash Reserve account which will offer one of the highest APYs in the industry.

How is it different from the Smart Saver product? It will offer a higher rate than many other savings accounts, have FDIC insurance up to $1,000,000, no minimum balance, no fees on balances and unlimited withdrawals (versus only 6 with most savings accounts).

The Checking account includes ATM fees reimbursed worldwide, no account fees, no overdraft fees, no minimum balance, and FDIC insurance up to $250,000. It also includes a bright blue Betterment Visa debit card.

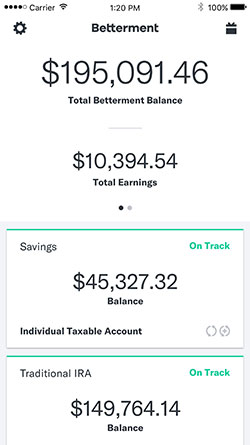

Mobile Apps For iOS and Android

Betterment didn’t have an app when they launched way back then, but they now have beautiful apps available for both iOS and Android.

Things you can do in the app include:

- Check the balance and returns of your portfolio in real time.

- Deposit and withdraw money anywhere, any time.

- Manage your portfolio’s stock and bond allocation.

- Review your goals and account activity.

The apps have only gotten better since they were released, and now support PIN login, management of your portfolio, and reviewing your goals anywhere on the go.

Fees And Charges

Here is where the rubber meets the road – what kind of fees and charges can you expect for using Betterment vs. Vanguard or some other low-cost investment company?

There are no minimums to invest, and there are no fees for trades. Betterment has three plans now, a Digital Plan, a Plus Plan, and a Premium Plan.

- Digital Plan: The plan that most people will end up using, the Digital Plan, charges a flat pro-rated yearly fee that is 0.25% for all users regardless of your account balance.

- Plus Plan: If you opt for the Plus Plan, where you get access to a team of CFP® professionals which includes an annual phone consultation. The cost is 0.40% annual fee (with a $100k account minimum).

- Premium Plan: The Premium Plan gives you unlimited phone consultations with the Betterment CFP® professionals and costs 0.50% annual fee per year. It carries a $100k account minimum.

Here is how they explain it on their FAQ:

Our Digital plan costs just .25% per year and offers unlimited access to automated portfolio management, tax efficient investing features, personalized financial dashboards and award-winning customer support. This plan has no minimum balance requirement.

If you’d like access to our team of CFP® professionals and licensed financial experts, you can elect into our Plus plan for .40% per year, which makes you eligible for an annual phone consultation as well as proactive account monitoring by our team of licensed experts. This plan requires a minimum balance of $100,000.

If you need more than one consultation per year, you can elect into our Premium plan for just .50% per year, which makes you eligible for unlimited calls with our team of CFP® professionals and licensed financial experts. This plan requires a minimum balance of $100,000.

NOTE: All accounts also now get tax-loss harvesting at no additional cost and no minimums. Previously there was a $50,000 minimum for this service, but that minimum no longer applies after Betterment removed the minimums for tax-loss harvesting a while ago.

The fees for Betterment originally ranged anywhere from 0.3% up to 0.9% annually when they launched. For many folks that was where they probably stopped reading, as having a 0.9% fee on account balances would be far too high, especially for folks who are more versed in the stock market and have confidence that they could buy a target retirement fund, or low fee index fund via Vanguard or similar low-cost mutual fund company. Going with a low-cost provider like Vanguard would mean a much lower cost because when you do it yourself there are no management fees. Depending on the balance that can be quite a bit of money you’d be saving by doing it all yourself.

Thankfully Betterment quickly reduced their fees from the high .9% for most folks with low balances, and it is now only .25% for most folks, which is very competitive for what they provide, and in line with many other providers.

Conclusion

Betterment.com launched at the end of 2010 and has received a ton of good press and accolades for its innovative investment platform. I have to admit that I am impressed with how they have taken a difficult subject – investing – and made it much more accessible to the average person. The fact that you can make automatic investments, allocations are automatically adjusted, and that it can be a cost-effective option for some investors with smaller amounts to invest make it an attractive offering. Betterment returns promise to be as close to matching the market as possible.

All in all – I think Betterment will be a great offering for many folks who are investing smaller dollar amounts, and who don’t want to do all the legwork and regular reallocation of assets. If they want a set it and forget type account, Betterment should probably be one of the first that they consider. And now that they’ve got a bonus just for signing up, I think there’s really nothing to lose! I’ve signed up myself, and now have about $20,000 invested with the service.

Signup Bonus When You Open A Betterment Account. Click Here.

Have you used Betterment.com, or are you considering it? Tell us your thoughts on Betterment in the comments!

| Robo-Advisor | Assets Under Management (AUM) | Annual Fee | Account Minimum | Bonuses | Review |

|---|---|---|---|---|---|

| Betterment | $15 billion | 0.25% of account balance. 0.40-0.50% w/ human advisors | None | Up to one year managed FREE | Review |

| Wealthfront | $12 billion | 0.25% of account balance | $500 | $5k managed FREE (Bible Money Matters readers) | Review |

| M1 Finance | $1 billion | FREE (fees for add-on services) | None | Review | |

| Blooom | $3 billion | $10/month any account size | None | FREE 401(k) Checkup | Review |

| Axos Invest | $153 million | 0.24% of account balance. | $500 | Review | |

| Acorns | $1 billion | $1/month under $5k. 0.25% of account balance above $5k. Free for college students. | None | Review | |

| Public | FREE | None | Free stock up to $15 | Review | |

| Stash Invest | $600 million | $1/month under $5k. 0.25% of account balance above $5k. | $5 | $5 New Account Bonus (Bible Money Matters readers) | Review |

| SigFig | $120 million | Under $10k FREE; 0.25% of account balance above $10k | $2,000 | ||

| Personal Capital | $8.5 billion | 0.49% to 0.89% of account balance | $25,000 | Review | |

| Wealthsimple | $5 billion | $0-$99,999 0.50%/yr; $100k+ 0.40%/yr | None | Up to $10k managed free (Bible Money Matters readers) | Review |

| Charles Schwab | $15.9 billion | FREE (They require you to hold 6-30% of portfolio in cash) | $5,000 | ||

| Fidelity Go | N/A | 0.35% of account balance; | $5,000 | ||

| Vanguard | $101 billion | 0.30% of account balance | $50,000 |

Betterment

Pros

- Easy to use

- Proven methods

- Low cost

- Automatic re-allocation

- Tax efficient investing

Cons

- Fees higher than DIY

{kind=link}

“For many folks this is where they’ll probably stop reading as having a 0.9% fee on account balances would be far too high”

I didn’t stop reading but I lost all interest right then. That seams pretty high for what it offers. The features it offers are pretty basic, IMO. In some cases you can find a full service financial advisor for around 1%. I guess if I am paying that much I would rather have someone I can meet with in person if desired.

When I was on there website I found it a bit weird that they were comparing themselves to a bank. Saving and investing are drastically different things because of the risk of loss associated with investing.

Great review, keep up the good work.

Hey Chris,

Jon Stein, Founder and CEO of Betterment.com here. We’re making investing easier and more accessible for busy people.

Betterment is an investment account. The accessibility we offer makes Betterment more similar to a bank account than other investment accounts are similar to a bank account – other investment accounts that have minimums, lock up your money for a certain amount of time, or charge you for every trade – on the way in and on the way out.

What more accessible means, to me, is that you can get your money back at any time – without paying a transaction fee – and without a minimum balance requirement. So you never have to worry. And that’s why I think the comparison to online savings accounts is helpful.

Of course, there’s risk in investing, and your principle is not protected. Betterment is not a bank. It is an investment account. You’re right to point that out, and we do the same.

On fees, the “full service” advisors you talk about typically don’t do anything more valuable than what Betterment does – they just charge more. And they have minimums of $50,000 to $500,000 – making them less accessible to most Americans. Our fee is quite reasonable considering the the ease of use, accessibility, and automation we provide.

Thanks for reading,

Jon.

Jon,

I appreciate that you’ve developed a platform for investing for the general public with no minimums. I’m sure that a lot of retail investors will be able to take advantage of it.

Out of curiosity, do you change investment allocations or holdings on a discretionary basis?

Hi Derrik,

We never change your investment allocation – that is solely up to the consumer. However, we will make allocation recommendations based on each individual’s goals and risk tolerance.

We passively manage the portfolio like an index fund, but we actively monitor it to ensure that we are always bringing our customers the best ETFs possible. Our goal is to grow with the market, not to try and beat the market – we believe this is the healthiest way to invest.

-Alan

VP Marketing | Betterment.com

Thanks, Alan.

So would it be fair to say that once the client has chosen their desired equity allocation percentage that your role is allocate that equity choice into the right percentage of equity asset classes (large, medium, small, value, growth, international) within the best ETFs that are available?

Derrik

Hi Derrik,

If I am understanding your description correctly, I think how you have framed it is a pretty good way to look at us. One note: we currently are not invested in international, but will be soon.

I hope this was clear, but everyone reading this should also feel free to email directly at alan@betterment.com any time questions arise – I will do my best to be as responsive as possible.

I hope this was helpful

-Alan

Well, I took the plunge and opened an account today. I’ll be playing around with it and reporting how I like it over the coming weeks. Stay tuned!

Peter, welcome to Betterment! We’re so glad you’re giving us a try. Let us know if you’ve got any questions or suggestions to make the product better.

– Jon.

unrelaistic that you will no trade for 6 years– and reallocation is inevitable at least once or more a year– that requires monitoring and selling– your asset allocation will be off for at least 10 months— and that requires commitment and discipline

in all, what you have described as simple is not that simple— thats why betterment can be a real good choice for most…

consider betterment as an allocation in and of itself– and you can still trade on your own with another percantage of your funds..

keeping some cash is also good..

As a person who is interested in investing and yet overwhelmed by the enormity of the research and time required to properly invest, I have found Betterment to be an excellent beginners product! I love the ease and simplicity the site and can’t wait to see where this all goes (hopefully up up up).

I know most discount brokers charge a fee for transferring out (typically $50 to $100), and I can’t seem to find this anywhere on the Betterment website. Thinking of signing up but worried that I could get slapped with a steep transfer out fee later on.

Does anyone have this information?

My understanding is that the only fee you’ll ever be charged is the annual fee of .15%-.35%. No fee for transferring out.

I want to bring this to the attention of clients of betterment that betterment charges a fee up to $400 if you want to do a direct (in-kind) transfer from betterment to another brokerage. I have been trying to do a direct transfer of Roth IRA from betterment to another brokerage firm and was quoted this amount.

This fee is also listed in their customer agreement in section 23. Please be aware that your only option could be an indirect roll over if you don’t want to pay $400 in transfer fees.

Betterment does not openly advertise this fee, which I think they must do when they list any or all fees on their website.

Katherine from Betterment commented on another site about this:

So there you go.. Sounds like there is a fee for a direct, but not indirect, rollover.

UPDATE 2015: There is no longer any fee for this. Betterment responded to our inquiry about this fee:

In the past, to perform a transfer out request it was an extremely manual process for us. We have since developed more robust systems that allow us to complete these requests with ease. To clarify, although we had this fee at one point it was never assessed.

Additionally, we have updated our customer agreement since then. If you would like to view our recent customer agreement, see here: betterment.com/customeragreement . On page 57, it reads “The fee provisions of the Brokerage Agreement and Advisory Agreement notwithstanding, there will be no charge for transferring Assets to another broker-dealer.”

Forgive me, I’m new to this whole investment thing and an independent investment advisor suggested I try Betterment rather then employ him at this time given the small amount I have to invest right now. But from the reviews I’ve read it looks like this is a good option for someone like me who knows nothing about the stock market and has a small amount to invest but that once you have over $50,000 it’s better to transfer to something where you have more control over the funds you are investing in. So in reference to the above question about the $400 transfer fee, I don’t know what you mean by direct or indirect transfer? If I want to open a Roth IRA with Betterment and transfer it later to another brokerage or online DIY brokerage is that going to cost me?

I agree that using a service like Betterment may be a good plan if you have a small amount to invest right now. Since they have no minimums, it’s a good place to start. I might argue that it would still be a good place to invest even after you’ve reached $50,000 – possibly even better because of their tax loss harvesting and other features.

Direct transfer and indirect transfer refer to how your funds are transferred out – either via a direct funds transfer to your new brokerage, or via an indirect transfer where they transfer your money to your linked account, and then transfer the funds to your new broker via your own bank account within 60 days. You should be able to do that without fees. My understanding is that as of 2015 you can only do one such transfer per calendar year, so if you transferred it out, you’d have to wait til the following year to transfer it again.

In regards to fees for doing direct transfers to another brokerage, my understanding is that there is no longer a fee. I reached out to Betterment and they responded that this was the case:

I keep putting $100 or so in Betterment with frequency. Then I just forget all about it which seems to be the big advantage. You just contribute and ignore it once you have your allocation right. Best formula- subtract your age from 100– that is the percentage that you should be in stocks

Been w/ Betterment since Nov ’14 and am quite pleased. Good svc. and they keep me informed.

Glad you’ve had a good experience with Betterment as well!

I have studied investing until my head explodes and I find Betterment to be the best option under most circumstances. I do take issue with having to invest so much internationally but over time I find myself trusting their research. I guess it is home bias. My wife even understands it to some degree and she is someone that needs to invest her money where she feels safe and I think Betterment does that for her.

I’ve opened up a Betterment account and I can vouch for the ease of use. It is literally, deposit your money and watch it grow. Since I’ve opened my account 3 weeks ago, I’ve already earned 6.7% on my Roth IRA. I would recommend this site for any novice investor.