Dave Ramsey is beloved around the world, and his Baby Steps have helped thousands achieve financial freedom. See 4 things we love and 4 things we would change.

Financial Peace University (FPU) Review: The New Updated 2012 Membership Kit And Class

Financial Peace University has been used by millions to escape the chains of debt. This month a newly revised version of the class was released. Here’s what is changing.

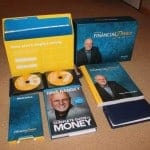

Unboxing The New 2012 Financial Peace University (FPU) Membership Kit

Dave Ramsey has just released a new and revamped Financial Peace University class. Today we’re unboxing the new membership kit included with the class.

Financial Peace University: Is It Worth The Price Of Admission?

Is Dave Ramsey’s Financial Peace University program worth the price you’ll pay to take it? Have you paid for the program, and if so, what did you think?

Dave Ramsey’s 7 Baby Steps Review: Is This A Debt Management Plan You Should Try?

The 7 Baby Steps is a debt management process popularized by Dave Ramsey and taught in his Financial Peace University class. Should you try it?

Dave Ramsey’s 7 Baby Steps Review: Get Out Of Debt, Build Wealth And Give.

This is a complete review of Dave Ramsey’s Baby Steps plan for getting out of debt, building wealth and giving.

Unintended Consequences Of Doing A Budget

Doing a budget has decreased our spending Within the past few months my wife and I have started doing a zero based budget where every dollar is allocated before it comes in. When the paychecks are deposited each and every dollar is assigned a job, whether it be paying bills, groceries, personal spending money or […]

A Way To Control Spending: The Envelope System

This past summer my wife and I took a class called “Financial Peace University“. The class is built around the teachings and personal finance framework put together by Dave Ramsey. Ramsey has made it his career goal to help people take responsibility for their financial lives, get out of debt, and save for their future. […]

Dave Ramsey’s Financial Peace University™ – Program Review

I would recommend The Financial Peace University™ class put out by Dave Ramsey to just about anyone who is interested in getting their finances under control.

Dave Ramsey’s Financial Peace University: Week 13 – The Great Misunderstanding

Last Week – Real Estate And Mortgages Last week was week 12 and we talked about real estate – buying homes and selling homes. Things we touched on: When selling a home, think like a retailer. When buying a home, think like an investor. Never get more than a 15-year fixed mortgage. Don’t tie up more […]

Dave Ramsey’s Financial Peace University: Week 12 – Real Estate and Mortgages

Last Week – Working In Your Strengths Last week was week 11 in Dave Ramsey’s “Financial Peace University“. Week 11 was all about careers and doing what you love for work. Ideas talked about: The average job in America is now 2.1 years in length. The key to power in our careers is to first […]

Dave Ramsey’s Financial Peace University: Week 11 – Working In Your Strengths

Last Week – From Fruition To Tuition Last week was week 10 in Dave Ramsey’s “Financial Peace University“. Week 10 was all about retirement, education and planning for the future. Key points: Independence in retirement is up to you. Don’t depend on Social Insecurity. Fund college education only after you are funding your retirement. If […]

Dave Ramsey’s Financial Peace University: Week 10 – From Fruition To Tuition

Last Week – Of Mice And Mutual Funds Last week was week 9 in Dave Ramsey’s “Financial Peace University“. Week 9 was all about mutual funds and other investment strategies. Some of the key points: The best way to invest is to be OUT OF DEBT first. Don’t put all your eggs in one basket […]

Dave Ramsey’s Financial Peace University: Week 9 – Of Mice And Mutual Funds

Last week – Clause and Effect Last week was week 8 in Dave Ramsey’s “Financial Peace University“. Week 8 was all strategies for negotiating, and using cash to reduce the cost of the items you buy. Don’t be afraid to negotiate. Be willing to walk away. Always use the power of cash. Remember the places […]