My wife and I were just asked by some friends at church if we would help them in hosting a Dave Ramsey Financial Peace University™ class at our church.

They had been planning to teach the class by themselves, but in the wake of our tough economic times they had over 60 people sign up for the class.

They decided they were going to need several other couples to co-host the group, and they asked us to be one of them.

We agreed to do our best to help facilitate the class.

Quick Navigation

Teaching Financial Peace University™

In preparation for our new class, I thought I’d do a quick review of our own experience in Financial Peace University™. So here is a review of the 13 week class.

Financial Peace University™ – Review

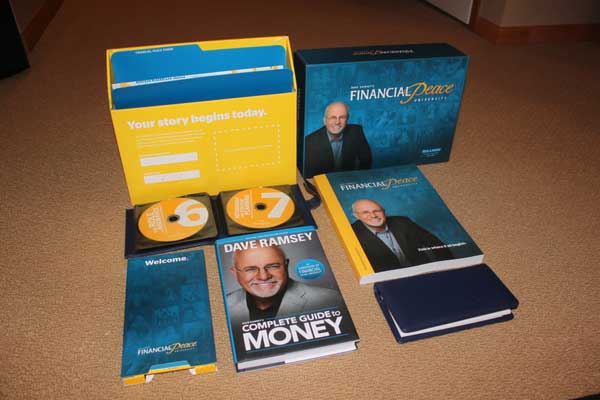

To start out, here’s a previous post looking at the FPU package that you get when you sign up for the program. In case you don’t want to check out the linked article, you’ll be getting audio CDs, CD-Roms, books, workbooks, cash envelopes and more. It is included with your class registration and fee.

- Unboxing Dave Ramsey: Opening the Financial Peace University™ Membership Kit

- Unboxing The Updated Financial Peace University Membership Kit

After we received the package from our group leaders we quickly jumped in head first and started reading Ramsey’s included book “Financial Peace Revisited“. It’s a great book for debt reduction, with plenty of insight and motivation. The program also has you read from the book each week during the class.

Starting The Class: Reviewing Where You Are, Relationships

When you attend the class for the first few weeks, it’s apparent that the focus starting out is going to be on setting a baseline framework from which to work for the rest of the weeks.

Before fixing your problems with debt, it’s important to know why you got into debt, talk about how you and your spouse relate about money – and how that may be different, and then look at how you can set up a framework to make changes going forward.

The class starts out looking at saving up an emergency fund to give you a nice base to work off of so that you don’t continue going into debt if some “emergency” were to happen. It also talks about setting up a larger emergency fund of 3-6 months once you’re out of debt.

Next the class looks at money in marriage, how our money affects relationships and how different people have different outlooks on money. They explore how that needs to be accounted for through having monthly budget meetings where finances are discussed.

Setting Up A Plan For Your Money

After communication about money is established the class dives into the important topics of cash flow planning and budgeting for your family.

It stresses the importance of assigning every dollar to a job (so money doesn’t just disappear), and shows you how to do a zero based budget in conjunction with the cash envelope system.

We set up our own budget recently using the software called “YNAB – You Need A Budget” which uses the idea of zero based budgeting and cash envelopes, but in electronic form.

Dumping Your Debt

After you’ve set up a budget, and have instituted the envelope system to cut your spending, the FPU class looks in depth at how to categorize and get rid of your debt.

It gives an in depth exploration of the debt snowball system in which you pay off your debts from smallest to largest. The system is great for motivating people to get out of debt by giving them small wins, and keeping them on the path to debt freedom. It also explores ways to create new income – even temporarily – while you pay off debt.

The program also talks about the use of credit, how it has gotten out of control, and how they believe that you should forgo the use of credit altogether – especially for those who are in debt.

Making Responsible Purchasing Decisions

The program also spends a week or two looking at how class participants can make better purchasing decisions in order to stay out of debt, and find better deals in the process.

It looks at how companies sell to consumers, and helps tip people off to some of the sales tactics used and the psychology behind them.

It also looks at how to get a better price when you are buying, and how to negotiate a better deal. Those classes were some of my favorite in the whole series.

Planning For The Future

A whole bunch of the lessons right in the middle of the class are devoted to setting up a financial and life plan with your spouse.

The topics covered vary from buying insurance for your family (home, health, life, disability, auto, long term care) to investing and saving for your kids education. It looks at the many options, and discuss which options are the best and should be considered.

It also looks at buying and a home (What type of mortgage, how much can you afford, etc), the best ways to sell a home. It also has a week on considering your job and work life and what type of career you should be in. It talks about working in your strengths and finding a career that you’ll love.

The Reasons Why We Get Out Of Debt And Save

The final class – and throughout the 13 weeks one thing that is stressed is that you shouldn’t just be getting out of debt, saving and planning for retirement only for selfish motives. You need to be doing these things so that you can also focus on other more important things in life like giving to those in need, supporting people and programs that you believe in – and just being more giving in general.

When you’re drowning in debt it isn’t something you can really do, but when you’re out of debt and on track for retirement – it will allow you to live more and GIVE more.

Conclusion

The Financial Peace University™ class put out by Dave Ramsey and the Lampo Group is a great class that I would recommend to just about anyone who is interested in getting their finances under control, dismissing their debt, and moving towards a brighter financial future.

While there is a pretty decent investment in time since the class is 9 weeks long, and there is a lot of work involved as far as creating budgets, reading the book and workbook activities – it is all worth it in my opinion because the class is very motivational, and for thousands of people has helped to flip that switch to make a change.

The only caveats that I would place on the program surround the investing portions of the class.

While I think some of the advice is sound, I also think some of it is a bit dumbed down for the wider audience – and makes some assumptions that may or may not hold true (like a 12% return on investments). For the debt reduction and motivational aspects of the class, however, I think it is second to none. That, and Dave Ramsey is extremely entertaining to watch during the weekly videos.

Have you taken The Financial Peace University™ Class? Did it make changes to your life? Tell me your experience with FPU in the comments.

UPDATE: The Ramsey Solutions team has reached out and told us that due to the COVID-19 crisis, for the first time ever, they are now offering a free 14-day trial of Financial Peace University online. Check out the details here: FPU Online free trial.

{kind=link}

Congrats on the great opportunity! Sounds like it will be a great experience.

My community offered FPU earlier this fall, but I didn’t sign up for it because we are already debt-free except the house. I’ve read quite a bit of Dave Ramsey and watch his show, so I’m wondering if FPU would be worth the time and money.

What are your thoughts on this? I wouldn’t want to take the class and not learn much… or worse yet, have the rest of the class hate me. :-)

Personally I thought the class was good, and entertaining even if you are out of debt. We were out of debt except the house as well when we took the class, but we still learned quite a bit.

Ramsey also has a very entertaining approach to teaching in the videos that are shown in class, so I think it would be worth it to take it anyway.

I agree with you in that Ramsey is a great teacher and communicator and definitely entertaining (after all I actually watch him on the Fox Business channel and how many financial experts could you say that people actually want to listen to!) but there are at least 2 areas where I think that Dave Ramsey is absolutely positively dead wrong. They are…

I used the snowball, i had a lot of debt, paid it all off in full no settlements.

This should be a lot of fun. I’ve yet to take a class myself, but would love to attend one with my wife here soon. We have been to a live event, and enjoyed hearing Dave reinforce the ideas we live by every day!

Frugal Dads last blog post..Is Cash Still King?

we had our first class last night, and we had a good group. Should be a lot of fun!

Is this a course that is offered in the states or is it available in Canada as well? Sounds like a good course for my Church as well.

I’m sure some churches in Canada probably offer it, and setting one up at your church shouldn’t be that hard. We just did that at ours.

In looking at the Dave Ramsey class finder it looks like some Canadian provinces are included, so you may be able to find a class near you.

You can also listen to his radio show on itunes if you’re interested, just do a search for Dave Ramsey.

@Pete

Are you really on step 3 or are you using debt to float your monthly expenses? (ie are you using credit cards and paying them off each month?)

yes, we’re really debt free – we’re not using debt to float monthly expenses. If expenses come up we pay them in cash.

I don’t quite follow his “no credit cards, only debit cards” approach. That would keep me from wanting to lead such a class.

Of course I am far from even staying faithful to his goal, so I wouldn’t be the best candidate either.

Brad

The idea behind the no credit cards approach is that when you “use credit”, you’re never really getting ahead. You may think you can use credit responsibly, but then – as ramsey says – Murphy comes calling. Everything that can go wrong, does. Credit cards you had intended on paying off right away end up carrying a balance. And savings becomes a second priority.

When you don’t use credit you’re able to be more responsible about spending, saving up for purchases before you buy them. You save up an emergency fund – just in case bad things DO happen. You get the appropriate health, life and other insurance to cover the worst case scenarios, and when you’re done making following the plan – you really don’t need to use credit.

Another good site to read about the whole – “we don’t need debt” paradigm is No Credit Needed. Thanks for stopping by!

I have no problem with the principle, I just don’t trust debit cards as much as he does and I have too many things that need remote authorization and such.

His points are great and I need to be truer to them, but I still don’t trust debit cards enough to switch completely there (especially after research into that area).

Brad

Hi,

I was just browsing the web about the new (2006) version of the FPU dvd’s. I have been a BIG Dave fan since 2002. I have paid my house off, have my emergency fund and have been putting over 25% of my income in investments. It took some work, but it was worth it. Its really nice to not have the burden of debt. In the financial meltdown we are in, I feel very secure. Even if I lost my job, I could still get a very low paying job and would be able to survive with no problems. I owe it all to Dave and I also feel that I have more than I deserve.

Just thought Id share that with you! It does work!

Brunswick, Maine

Instead of asking for a handout, why dont’ you try saving like $5-10 per week and save up for the class? We all have misc expenditures that we can cut back on to get something we want. Think of it as practicing savings before you even get in the class.

We’re doing FPU right now and hoping to bring it to our church in the Spring. So far we’re really loving it, and we’re taking our eleven year old daughter along (with a calculator and a workbook so she can follow along on the math too!)

Jessica W´s last blog ..This Saturday 9/26 Free Museums Day!

I’m a twenty-three year old tradesmen from Canada, thanks to Mr. Ramsey my fiancee and I are on the verge of having all of our wedding money saved up. We were lucky enough to find out about Dave Ramsey when we were still very young and because of that we avoided a lot of the traps a young couple can fall into finacially. For anyone who is in doubt about Mr. Ramsey’s system believe me I am living proof that it works and works well.

How do I find a local Financial Peace University Program.?

Located in Orange County New York.

Local Zip codes are 10950; 10924; 10940; 10918

I am interested in attending a class with my husband we live in whitby ontario not sure if anyone knows of any meetings we can sign up for?

What’s so bad about having a mortgage? As I’ve paid mine down, I’ve refinanced numerous times and used that money to build wealth by buying investment real estate, 2 businesses and other investments. The passive cash flow I receive from these investments covers my lifestyle, easily including a mortgage payment, and allows me to support a challenged child, my church, 2 missionaries, several local charities, and brain and breast cancer research. I will continue this cycle, repeatedly harvesting equity from all properties/assets, and expand its reach until I am not mentally capable of doing so, and then the ideal will live on through my trustees.

A mortgage (debt) is one of the most powerful wealth-building tools in your financial toolbox. There’s good debt and bad debt. If you’re not responsible or disciplined, then debt could be a bad thing. In my opinion, it should never be used to fuel consumption, which has been encouraged by banks and credit card companies for their profit, not their consumers. But it can very effectively be used to build true wealth, which would be much more difficult if you tried to save your way to it. After all, who do you know who has saved up enough to pay all cash to purchase their home?

If you like, read The Fiscal Fitness Letter’s ‘Debtor vs Saver vs Wealth Creator’ for a different perspective and cycle for wealth creation.

I believe locking up a few hundred thousand dollars as un-performing equity in a home is wasting a resource that should be put to work for the greater good. It’s like the 3rd servant in the story of the talents in Matthew 25, who buried his share out of fear and did nothing with it. In faith, we can go forward and optimize our assets, cash flow and liabilities, confident our good stewardship will be blessed and we will be able to be rich in good deeds, generous and willing to share (1 Timothy 6:17-19). None of what I have will I take with me, but I can leave it better or greater than when I first received it.

Scott, what a wonderful statement “None of what I have will I take with me, but I can leave it better or greater than when I first received it.” I truly believe that also. God Bless.

There isn’t much mention of paying a tithe seems kinda strange. Being a good steward of the money God gives you is important but giving back is equally important.

Actually he does talk about the tithe in the class, although I didn’t touch on that in this post. His advice is to pay the tithe – the first 10%, and he stresses giving in the class – the last session is all about giving and how important it is..

Our church is offering this course…starting in 2 weeks. My husband and I are in our 50’s and have struggled financially our whole married lives, and are far from being debt free. I am interested in taking this course but have a few concerns: 1.) I would have to attend alone as it is being held during the week and my husband is only home on weekends due to work…is this a class that both partners should attend together to reap the full benefit?

2.) being in our 50’s…is it too late for us? My husband is talking about finally following his dream of opening his own plumbing company, but we need to be in a better place financially.

3.) We are new to this church, so my attending alone will be slightly overwhelming to me…speaking in a small group setting about something so personal as our finances, without my husband there will be difficult to say the least. Just wondering if we’ll actually get the full benefit of the program?

Any advice/suggestions you might have would be greatly appreciated.

Thanks!

1. I think it’s best if you can both attend the class, but it’s still possible to take it without both there. You may want to see if the class organizers will have the FPU videos available for checking out so that you can bring it home and your husband can watch it. If not, when you sign up you’ll also be getting the FPU packet which includes the audio of all class sessions. So he’ll still be able to take part without being there even if it’s just listening to the session.

2. I don’t think it’s ever too late. When we took the class there was a couple in their 60s in the class that it helped greatly. No matter what your situation it can help to get you in a better place financially.

3. I think the class works best when you’re able to share with those in your small group. There are plenty of other folks who are likely in similar situations to you, and everyone is there to help improve their situation. So I think the atmosphere is one that is supportive and helpful. For us it was an atmosphere conducive to sharing – even if it isn’t always easy.

Good luck!

Peter,

I am in my 60’s, swamped with about $55,000 in debt, no money saved, and just about to take a well paying job, but need structure as to how to start attenuating all this debt, and save for the future,as well as setting up all the Insurances I need to protect against unexpected things of life.

I am starting Baby Step 1 of Dave Ramsey’s FPU.

Got any additional insight a s to how to tackle this load I am carrying?

Lastly, I’ll need a transportation car to get me to and from work and Church. What do you think I should spend on a car with a salary expectancy of 30-45K annually?

Blessings.

Where can I find some testimonials to be used for an advertisement for an upcoming FPU?

Mike,

I just stumbled on this website and have went through FPU about 8 years back. I’m at baby step 7 and living and giving like no one else. As far getting testimonials you can go to Dave Ramsey.com, Dave Ramsey on Facebook and Dave Ramsey’s Twitter page. You can get promotional materials there as well you can sign up and get a sponsor to help get you started and guide through hosting a FPU class. I recommend reading Peter Anderson’s comments.

Good Luck,

Could someone use the old workbook in the 2012 class? For instance, if a couple took the class and had the kit, but one spouse wanted to have their own workbook?