When it comes to your retirement, there is a very real chance that you could be sabotaging it. When it comes to your real returns, you need to be vigilant about offsetting the effects of inflation, and avoiding overpaying with your taxes. Many investors realize this. However, there are many investors that, at the same time, don’t realize they are paying too much in fees.

It’s impossible to completely avoid all investing fees. There will always be fees to pay when you invest. But chances are you are paying too much. A recent study indicates that a typical two-income household will pay more than $155,000 in 401(k) fees over a lifetime. Another study, from Vanguard, suggests that up to 29.6 percent of your investor returns might be eaten up by fees over the course of 10 years. That’s pretty close to a third of your returns swallowed by fees — instead of in your account working on your behalf.

Retirement plans often come with a host of high fees, and chances are that there are high-priced funds involved as well. Combine plan fees with the fund fees, and you’re looking at thousands — tens of thousands — of dollars. What if you could avoid some of these fees and put more of your money to work for you?

Enter Rebalance IRA, a retirement portfolio investment service available at a portion of the standard industry cost. You’ll get better results, and pay less to boot.

Personalized Investment Help for a Low Cost

Rebalance IRA takes a look at your current investment situation, looking at what’s in your IRA (or the 401(k) that you rolled over to an IRA) and helping you decide what needs to happen in order for you to reach your long-term investing and wealth goals.

Because studies indicate that asset allocation is an important part of long-term investment success, Rebalance IRA uses an asset allocation strategy that falls in line with Modern Portfolio Theory (MPT). Asset allocation using MPT involves dividing your portfolio between S&P 500 companies, bonds, small company stocks, foreign stocks, and real estate. Rebalance IRA accomplishes this asset allocation, for the most part, without picking individual investments.

Since studies indicate that asset allocation is more important that individual investments, it makes sense to focus on funds. By using low-cost funds to create a portfolio that is properly balanced according to your own risk tolerance, Rebalance IRA is able to offer you a superior portfolio at a fraction of the cost you would pay at large brokerages — or even with your own company’s 401(k) plan.

Once Rebalance IRA reviews your assets, knowledgeable advisors, all of whom are Registered Investment Advisors (RIAs), help you identify problem areas. A plan for your portfolio’s long-term success is then created on your behalf.

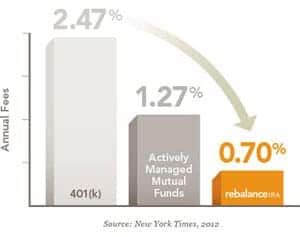

You can set up a free consultation with one of Rebalance IRA’s investment advisors to get an idea of what the service can do your behalf. If you decide to proceed, your fee is 0.70 percent annually. That’s not bad when you consider that many actively managed mutual funds charge 1.27 percent or more a year, and that it’s not uncommon to find company 401(k) plans that charge up to 2 percent or more per year.

You can set up a free consultation with one of Rebalance IRA’s investment advisors to get an idea of what the service can do your behalf. If you decide to proceed, your fee is 0.70 percent annually. That’s not bad when you consider that many actively managed mutual funds charge 1.27 percent or more a year, and that it’s not uncommon to find company 401(k) plans that charge up to 2 percent or more per year.

Another nice thing about Rebalance IRA is the fact that RIAs have a fiduciary duty to their clients. That means that their recommendations — by law — have to be in your best interest. Rebalance IRA doesn’t charge transaction fees or commissions, so you know there is no conflict of interest in the recommended investments. Instead, you just pay the low percentage of assets in your account. It’s a low fee that means more money for you to keep and put to work earning interest.

You do need $75,000 in order to open an account with Rebalance IRA, though. This is a service designed to help people who are already building up their nest eggs; it’s not aimed at people just getting started with retirement investing.

Don’t Get in Your Own Way

Chances are that, at some point, you will get in your own way when it comes to investing. Investors are irrational. We panic and sell when we should be buying low, and we get greedy and over pay for things when the market is doing well.

Rebalance IRA helps you avoid some of these pitfalls by taking over for you. One of the great things about Rebalance IRA is the Investment Advisory Board, which helps set the tone for the entire operation. The cofounders of Rebalance IRA, Mitch Tuchman and Scott Puritz, are former financial industry insiders who understand investing, behavioral finance, and investing. The advisory board also includes these three investing luminaries:

- Dr. Charley Ellis: Dr. Ellis sat on the Board of Directors for the The Vanguard Group, and is a form of the Yale University investment committee. He’s been on other governing boards for prestigious business schools. He’s also the author of Winning the Loser’s Game, a bestselling book about investing.

- Dr. Burt Malkiel: Most investors are acquainted with Malkiel’s book, A Random Walk Down Wall Street. He is a well-known financial writer and has also been on The Vanguard Group’s Board of Directors.

- Jay Vivian: Vivian managed IBM’s Retirement Funds, overseeing $135 billion in investment funds for IBM’s 400,000 employees around the world.

As you can see, investments used your Rebalance IRA portfolio have been carefully thought through, the philosophy is directed by people who know what they are doing. You can benefit from this expertise without paying a hefty sum.

Rebalance IRA helps you periodically rebalance your portfolio so that it doesn’t get out of hand, and so that you stay on track. It’s a great tool for those who want to take a more hands-off approach to their retirement investing.

A hardcore DIY investor probably doesn’t need Rebalance IRA, especially if you are good about comparing fees, and you take the time to re-evaluate your portfolio every six to 12 months. However, if you want someone else to manage your retirement investments, it makes sense to consider Rebalance IRA for the expertise at a low cost.

It’d be better (in my opinion) to develop your own asset allocation and use inexpensive Vanguard funds (or ETF’s) and avoid the 0.7% fee. This seemingly small fee will add up significantly over time. If you need help setting up the asset allocation, consider using a fee-based planner instead. One small up-front cost and your system is set – you just need to follow it. Will it take a bit more emotional self-control? Yes, but your self-control can earn you an extra 0.7% per year! And (here’s the key) if your asset allocation is set up correctly up front, you’re not as likely to bail out when the market tanks (as it will certainly do periodically) because your allocation matches your risk tolerance (again, a fee-based planner can explain this in more detail specific for your situation).

John, the 0.70% fee is inclusive of all fund fees, and is the average. Their management fee is actually only 0.5%, which is half the industry standard of 1.0%. They do focus on low cost index funds and they don’t earn any commissions or sell actively managed funds. Depending on which funds are in your portfolio, your total cost could be closer to 0.6% (again, this is entirely dependent upon your investments).

I agree that managing your own investment portfolio is less-expensive. But not everyone has the desire, expertise, or discipline to do it. For those people, hiring an RIA (Registered Investment Advisor), with a fiduciary duty to the investor, may be a good option.