This past summer my wife and I took a class called “Financial Peace University“.

The class is built around the teachings and personal finance framework put together by Dave Ramsey.

Ramsey has made it his career goal to help people take responsibility for their financial lives, get out of debt, and save for their future. The class is a very good one, and I suggest you check it out if you’ve ever had problems managing your finances.

I loved the class so much that I’m now helping to facilitate a class at our church by helping some friends teach the next session of Financial Peace University.

One thing we’ve realized by teaching the class is that we’ve let our finances slip the last few months as we were out of the country for a few weeks and dealing with other various issues of life.

We just haven’t been doing our budget, and certain spending categories have gotten out of control.

If we were going to be teaching this class, and being a good example to others there, we figured we had better get things in order, and get our spending back in line.

So how to cut our spending?

One thing we neglected to do last time we took the class was to control our spending using what Dave Ramsey calls “The Envelope System”.

We figured we could do a “virtual envelope system” using the computer and money software like You Need A Budget or Dave Ramsey’s EveryDollar software.

We just never got around to it, and now we decided to give the actual physical envelope system a try.

The Envelope System – Getting Started With A Budget

The first thing you have to do when you’re trying to control your spending is to set up a budget.

If you don’t know where the money is going and what your set expenses are, it will be difficult to set up a working budget or envelope system.

Tracking our expenses was relatively easy because we logged pretty much every dollar coming in or out in You Need A Budget. We have a good 1-2 years of history right at our fingertips.

With that, we were able to see exactly how much we were spending on set expenses (mortgage, utilities, taxes), as well as other categories where the spending was out of control (food, shopping).

Once you’ve got a good baseline for what you need to spend every month on the basics, you’ll want to set up a monthly cash flow plan and give every dollar a name by doing a zero-based budget.

What that means is every single dollar of income that comes into the household will be allocated, and assigned a job. If you make $5,000 of net income, all $5,000 of that should be allocated either to an expense or savings category. That way you won’t have the extra money (after expenses) disappearing into the ether.

Every dollar gets saved, assigned to a debt, or gets some other job. Your money works for you instead of just melting away.

So to review, the first steps you’ll want to take include:

- Figure out your regular monthly set expenses.

- Figure out other variable expenses (like food, shopping, and entertainment) and assign a realistic dollar amount for that category in the budget.

- Put together a zero-based budget where every dollar of income and expense is allocated. Every dollar has a name and a job.

Setting Up Your Envelope System

Once you’ve got a budget setup, and you know how much you want to spend on each category, it’s time to setup your envelope system.

The idea behind the envelopes is that it helps you control your spending on certain problem categories by giving you a set amount of money each month in your envelope that you need to use towards that category.

When the money is gone from the envelope, you can’t spend any more money on that category.

If you absolutely need to spend more, you have to take money from another category to fill in the gaps.

We have a couple of big problem categories that we consistently overspend in. Eating out/restaurant spending and shopping spending.

My wife and I love eating out, and in some ways eating out has become our way to connect with each other and entertain ourselves. If we have a date night we go out to a nice restaurant and enjoy an evening together. The problem is that we’re doing it way too often, and spending way too much money doing it.

The solution?

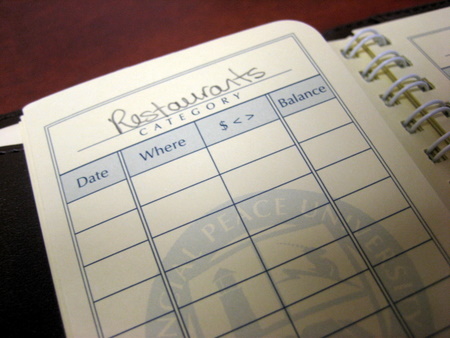

We added these problem categories to our envelope system. In the picture below you can see our envelope for “restaurants”.

We also set up envelopes for some other categories with variable expenses including groceries, shopping, entertainment, and “blow money” (personal money we can spend for every and any reason).

Whenever we get paid we are now going to withdraw money for each spending category and place that money in the envelope.

For example, if in our budget we allocate $400/month for groceries, we’ll withdraw $200 from the first of the month’s paychecks and put $200 in the envelope. Whenever we go shopping for food we can then only spend money from that “groceries” envelope, up until the point the money is gone.

If we go shopping and the bill comes up to $201, we must take that $1 from another envelope, or put back $1 worth of food. For the last paycheck of the month, we’ll once again withdraw $200 for food and add it to the envelope. If we’ve only spent $100 the first two weeks we’ll then have $300 in the envelope. At the end of the month, if you have money left over, decide how to allocate that money – either putting it towards debt or saving it.

Using this system may be a bit uncomfortable at first, especially if you’re using envelopes for a larger number of categories. We know of one couple who set up a ton of spending categories using this system and then ended up withdrawing thousands every month and putting it into envelopes. We decided it would be easier to just choose some of our biggest overspending categories and withdraw the money for those.

It comes out to about $800/month that we’re withdrawing and putting in envelopes.

The Basics Of The Envelope System

- Set up a zero-based budget, and know how much you should spend in all categories.

- Find some of your biggest over-spending categories, or places where the expenses vary quite a bit every month and set up an envelope for those categories.

- Every paycheck withdraw enough cash to fully fund the envelopes for your envelope system.

- Only spend what you have in the envelopes, and if you don’t have any money left , don’t spend. If you need to spend more, take it from another envelope.

- Any money that is left over, either save or put towards your debt snowball (if you have debts).

While we’re still setting up our envelopes, we know from watching others use the system that it can have a dramatic effect on how much money you’re spending. Not only are you setting limits on yourself and living on a budget, but you’re also spending cash, which hurts more.

Studies have shown that when you use a credit card, even if you’re paying it off every month, you spend on average 12-18% more.

Using cash for those problem categories will help you to rein in that spending, and force you to not spend more than you make.

What do you think of the envelope system? Are you currently using the system, and how does it work for you? Do you prefer physical envelopes or using “virtual envelopes”?

We’ve used the envelope system for 2 years

now and it works! We use regular envelopes

and 4 categories: Groceries, Gas, Household

Expenses(stamps,etc), and Entertainment.

When the envelope is empty, we’re done.

It takes discipline but it does work.

We deposit the cash into the envelopes twice

a month. Hubby thought I was nuts when I

first suggested we try this, but it didn’t

take long for him to see how useful it was

to do it this way. Try it and see how it

works for you.

We have virtual envelopes. I have different accounts for different things. It’s been working well for us. I keep track of it all on Quicken, and it’s very easy to create graphics to illustrate how “on track” we are.

I don’t do the zero-based budget, though. I like to have a little cushioning at the end of the month. So we have a budget based on having $300 left over at the end of the month. That way it carries over just in case a client is late with paying me (or doesn’t) and we need a little floater space in the main checking account. It prevents us from having to raid our envelopes and keeps me feeling better about our cash flow. Plus, it’s there if an emergency comes up, like this last month we had an unexpected expense, and it was nice to have that short-term cushion (built up for three months) to access, rather than having to go into the emergency fund.

Last month, I went all-cash for my spending. I hated it. I’m going back to using my debit card, with amounts allocated to different purposes.

I know envelopes are a good way to save money, but I don’t like feeling deprived if I run out of money in a category.

We’re spending less than we earn each month, so if I have to borrow money from one category to use for something else, I don’t want to feel like a total failure.

Kacies last blog post..Goals for November

I like the idea of the envelope system. I tend to use blank envelopes and don’t record on the envelope what is spent.

So I guess I use a partial envelope system.

My wife and I went to an FPU class as part of our pre-marital preparations, and it was a huge blessing! We also had the chance to attend a LIVE! event in KC this spring :-). We have been on a zero-based budget and the envelope system for about 2yrs now (married for 1.5yrs, so we had individual systems going for 6mo prior), and we LOVE it!! We wore out the freebie envelope system we got in class, and our deluxe envelope system from Dave Ramsey is showing some use :-). We do use a virtual envelope for gas since that is one thing that’s a real pain to do cash.

@ Kacie it takes time to get comfortable with a cash system. It took me about 3 months of just sucking it up to get it working right. So don’t feel like a “failure” you’ll screw up at least the first 3. And feeling “deprived” might be a good thing ;-). Most of our wasted spending is impulse and “needless” spending that could use a yank on the chain!

We have used the envelope system for over two years now. We only carry cash for items we purchase locally like groceries, restaurants, personal items, etc. For conveinence sake, we use a debit card for other purchases, but track these purchases in our YNAB personal finance software.

I am a big fan of the envelope system, but of course, the most important thing is to find a budgeting system that works for you.

Jeff@MySuperChargedLifes last blog post..Now Is A Good Time To Be Living On A Budget

I keep trying to find a budgeting software, and keep forgetting about YNAB. I have to remember to check that one out (how could i forget -i advertise for it in the sidebar? silly me)

We cannot make the envelope system work. Maybe we’re trying too hard to keep track. But often, my wife or I will stop and pick up groceries, household items, etc. We don’t have the envelopes with us. Then we loose track. This happened several months in a row and we finally gave up.

How does anyone make the practical parts of this work?

You just have to stop making as many “oh i’m on my way home so i’ll just stop” type trips. I know I do that alot, and it does tend to mess things up. If we do that, when I get home I’ll grab the money from the envelopes, and deposit it back in my account the next day (or at least that week.)

Here’s how I handle it. It’s not really a problem if you do it this way:

If I decide to go shopping without my envelopes, once I get home I pull the amount of money I spent into an envelope devoted to repaying my VISA purchases(which is what I use in preference to a debit card).

That way the cash envelope gets adjusted down, so I’m still working the system and can’t lie to myself about how much money I have left to spend, and the visa bill has money waiting for it when it comes due.

I have known about the envelope system since my college days back in 1979!! I learned about it though a friends who was involved with Campus Crusade for Christ. Its how they were taught to budget their money, so that they would not waste the money of the people who supported them. Its called being a good steward of the money that we are blessed with.

It works and after awhile we just got use to paying cash for groceries and gas and we learned to budget all the time. Now we just use Quicken (our virtual enevelope) to track everything. My husband and I get a monthly allowance to spend as we want…no questions. I don’t have to explain the $4.00 latte and he doesn’t have to explain the new tool for his workshop.

We’ve got that “allowance” or “blow money” built into the budget too. so now i don’t have to explain that new gadget – or video game!

Great Idea,

We’ve been doing really well with saving money without the envelope method, but I bet we could do even better with it. I think we do the best job of not eating at restaurants when it’s not a semi-special occasion. I have mostly been using my iCal on my mac and just tracking past and future expenses based on their dates. Great article!

The Geared Investors last blog post..Great Article Explaining Options and Benefits When Investing in Currency ETFs

I’ve used Crown Mvelopes for five years and love it! I can use my credit card, debit card and write checks and they will all show up in the program. I treat all of them, even my credit card, like cash. So if I have $50 in my clothing “mvelope” I only spend within that amount for clothing. If I use my credit card, the program takes money that is in the mvelope and transfers it to a special mvelope so that when the bill comes, I can pay it and have not spent it.

If I need to spend more than the $50 then I will look to see if I have some money in the misc. mvelope or maybe I did not have to spend as much on electric bill as I have budgeted so can take a little from the extra.

So now, I just make up a budget for each check and fund my mvelopes automatically. This way, if I need to put $52.50 in the home association mvelope every month in order to have the money ready when the bill comes, I don’t have to have exact change in a physical envelope and I don’t have to write anything down.

I have used the paper version of mvelopes but it is difficult to have all the physical dollar bills and be able to divide them every pay check. And if I kept the money in the bank and used only a roster, I never knew how much I actually had because my husband would go a couple places and not give me the receipts. With Mvelopes, I see every transaction when it clears.

We paid down the original credit card debt very fast and then kept out of debt. We had 4 pay cuts and we were able to see very easily where to cut back.

It is fantastic! Check it out

Once upon a time… I made a good living with plenty left over each month to invest, travel, etc. Plus, I could always pick-up side jobs to make extra if we needed. I didn’t do credit cards or have large debt issues, so that helped us live comfortably. UNTIL… I got sick. Had to sell the house & cars. Everything I invested over the years was gone to pay hospital/doctors’ bills. After surgeries & treatments I was still disabled & couldn’t work to earn that paycheck we had gotten used to. I was financially at ROCK BOTTOM!!! I had to quickly learn to live on a much lower fixed income & still pay the mound of debt. I STARTED THE ENVELOPE SYSTEM… only I used a coupon organizer. Sturdy plastic on the outside & unmarked, tab dividers inside to make my own catagories. I get 1 check a month, divided it into my catagories & left just enough money in the checking account to pay the “auto-pay” bills. People say… what if I see cheap gas & I don’t have the gas envelope? Or, what if I need to stop for groceries after work? No worries… I carried my ENVELOPE SYSTEM (coupon carrier) in my purse like a wallet. Even my kids knew when the money was gone from under that section, we were done spending & I got no fuss from them. So, 5 years later I still have health issues but makes it a lot easier when… I’m debt free… My rent has never been late & bills are paid on time each month. It may seem hard to get the budget at 1st, but I’m here to say the ENVELOPE SYSTEM saved me a lot of stress & got me on the right financial track… Life is good :-)

Actually I had a similar idea.

I want to ask the author, I do agree this is a great idea brut what if we could create envelope system in banks.

For example we could create multiple categories in chequing account in our Debit Card.

and We can use that category to spend the money. If we do not spend it will still be accumulated automatically in the respective accounts like, Food, Clothing , according to the budget we set aside each month.

We love the envelope system. We did this a lot when we first stating off on our debt reduction plan.

We are using the envelope system. You know when you talk about the psychology of cash, it really rings true. I feel like it is both the secret to why it works and also the secret to why people won’t do it or give up on the envelope system.

It was scary to use cash at first. I was uncomfortable. I remember being in the grocery line and I was nervous that I wouldn’t have enough. After you get over that 3 month hump of using the envelopes, it gets so much easier and it definitely works. My husband and I tried to just use our credit cards and sort of do categories before envelopes. We would always over spend. There is just something magical about pulling out the cash to pay that makes you decide to buy 1 box of spaghetti rather than 2 this week.

I love the envelope system so much I started making and selling my own sets on Etsy. https://www.etsy.com/shop/CraftySundays?ref=hdr If you get a chance I would sincerely appreciate you taking a look. Anyways, I love this article. I love reading about others successes with the system.

Let me know when you find some software that implements envelopes digitally, and is NOT online. Haven’t found it yet!