Over the next few months we will be taking a long and laborious journey through the perilous tax season.

But, some of you are giddy with excitement.

You think you are finally going to get something of value from the government – an income tax refund.

All year you’ve been waiting for this moment. Now you can finally afford to take a vacation or buy a new car.

Can I interrupt your dreaming for a dose of reality and a little reminder?

The money the government sends you is the money you already sent them.

Far too many people view a tax refund like manna from heaven. However, this is not God’s sovereign way of providing for you. It means that throughout the previous tax year you had too much money withheld from your salary.

Quick Navigation

Three Reasons Why A Big Tax Return Is Bad

- A big tax return simply means you did not properly calculate and estimate your taxes.

- A big tax return means that you let the government hold your money for up to 16 months. By the way, the government did not give you any interest on that money.

- We think psychologically different about found money than earned money.

Found Money Vs. Earned Money

Earned money is money you get on a regular basis that is closely associated with the work required to get the money. After working for two weeks you get a check from your company and say to yourself – you bet I deserve this, I busted my back to get this money.

When you sit down to budget earned money, you say to yourself – hey, I worked hard for this money I’m not going to waste it like water.

Found money is money you get on a one time basis (or very rarely) that feels like a gift. This unexpected income must always be budgeted or you are likely to spend it without control. You work all year and pay money to the government and you “forgot” you were sending them money every month. When you get a check (tax refund) in the mail, you say to yourself – party time, I forgot I had this money. What’s the best way to blow this money?

The only problem is that this found money is really earned money.

You will spend your money a lot more responsibly if it is not withheld from your pay check.

What Is The Financial Cost Of A Big Refund?

How about the financial cost of a big tax return?

Let’s say you had an extra $4,000 withheld from the previous year. Simultaneously, you’ve been paying down debt. You have a $4,000 credit card debt that charges interest at 12%. This means that you paid around $500 just so the the government could keep your money and send it back at the new year.

This, my friends, is not a financial plan. It is a financial disaster. If you’re getting a big income tax return, I encourage you to adjust your income tax withholding. Keep your earned money.

How To Adjust Your Income Tax Withholding

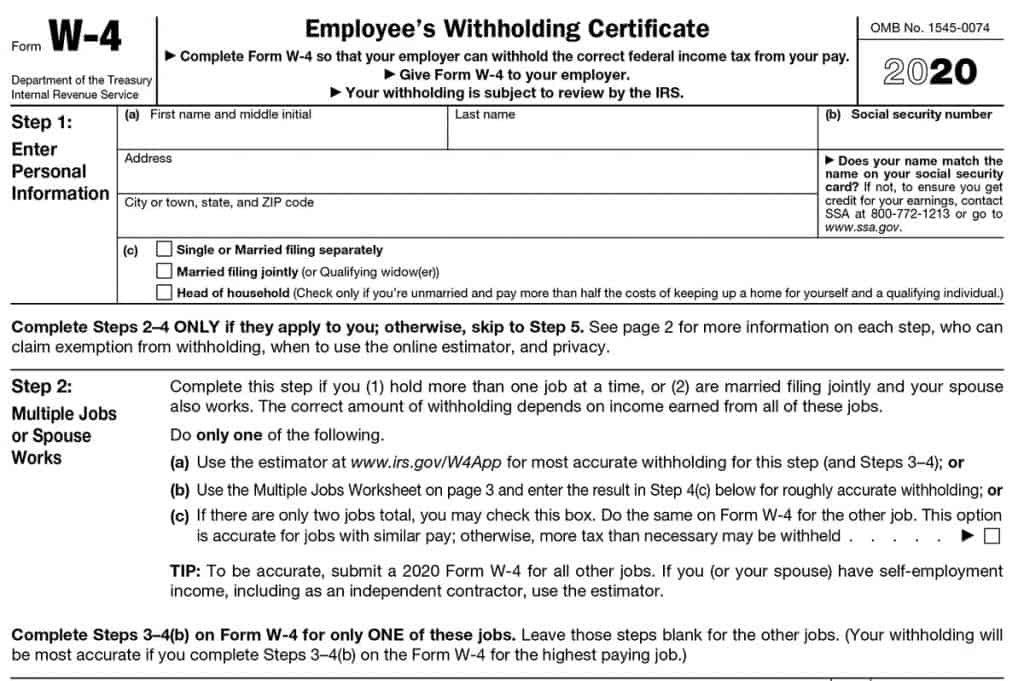

- If you are self employed just make your estimated quarterly payments based on what you should have paid last year (this assumes your financial and family conditions will remain the same).

- If you are employed you will need to visit your HR representative and get a new W-4. The W-4 tells the company how much to withhold from your pay. Make the necessary adjustments to dependents in order to get the withholding to match tax liability from the previous year. The goal is not getting the number of dependents right, but getting the withholding right. More details here.

Do any of you like the idea of getting a big tax refund? Do you use the income tax refund as a forced saving plan? Have you considered changing your withholding to make sure that you don’t get a big refund? Tell us your situation in the comments!

I actually changed my withholding in October to add 10 allowances (!), but sitll came about $600 short, so I’ll be getting it in a refund. Of course I would have liked to have had it earlier, but it would have earned about 2% in a savings account.

2% of $600 is $12, which isn’t a big deal. Not to mention that I only worked the second half of 2009, so that 2% is really 1%. But I didn’t send in too many payments until September or October, so it’s really more like 0.5%, or about $3. Not a big deal at all.

I now have more of a financial plan so I’ll be using it to fund my 2009 Roth IRA. Unless you are withholding WAY too much, I don’t think it makes much of a difference.

The advantage for some people is that they think they’ll do better if they used a forced savings plan. But what makes them think that they’d be irresponsible if they got it with their regular paycheck but if they get a lump sum they’ll suddenly be very responsible?

Daniel´s last post ..What is Financial Success?

People LOVE getting a large refund. Some to the point where they don’t want to hear that they can have the money earlier. I used to feel that way but I’d much rather have the money in each paycheck then wait to get my free loan back. The money can be better used under my control.

FFB´s last post ..New Financial Tools Make It Easier to Plan for Retirement

When I was a student and my tax refund was really wealth redistribution, it was great. That money really was found, because we were poor and had the EIC and the Additional Child Tax Credit. But now – not so much. So we try to figure out tax liability quite closely, and not overpay. Because that money could be working for us, rather than languishing in government coffers without earning a return.

Miranda´s last post ..Reader Question: How Much Life Insurance Do I Need?

The main reason our family receives a large refund is because we have 3 children, and only one income. We receive barely anything “back” from my husband’s salary.

I WISH we could use this refund for a vacation or something fun, but we put it back in our emergency fund (a’la Dave Ramsey), and use it to pay off some of our debt. We MIGHT use $50 to go out and eat and see a movie, but that doesn’t happen very often!

Amy @ Amy Loves It!´s last post ..WW: Mommy’s Wedding Dress

I should be getting a refund, I don’t consider it large, but it is a significant amount…enough to make a dent in a debt payment. I’ve thought about adjusting the amount withheld, but when divided by 26 paychecks in a year it really doesn’t increase the bottom line that much. In fact, my risk is probably higher of messing something up and owing money come tax time. For now, I am in a “comfort zone” with my tax refund situation.

My approach is probably elementary but it works for me…for now. As I go through life and situations and circumstances change, I’ll probably revisit this.

Thanks for the reminder!

Kita

I hear you completely on the point of this post.

It is probably the last big thing I need to do. it just seems to me that by having a large amount withheld, I am forced to get by on less throughout the year, which in turn saves more money.

My entire tax reutrn is invested, and I fear that if I change my ways, that I’ll find way to spend that money

David/Yourfinances101´s last post ..Blogs o’ the Week

Don’t listen to Craig

Just keep

Doing what you do.

Craig is obviously just voicing some opinion.

But it is ok. He can do that even if he is wrong.

Ughhh I could not agree more with you, however, my husband refuses to change our withholdings. We get back such a ridiculous amount that I am embarresed to even say it. I have tried for several years to change this, but he is so afraid of oweing money that he wont. I may just email this article you wrote to try and convince him. Pray for me :)

@Daniel

I love the question you asked, “But what makes them think that they’d be irresponsible if they got it with their regular paycheck but if they get a lump sum they’ll suddenly be very responsible?” If I can’t be responsible with a montly trickel of money can I expect to be responsible with a lump sum in the new year?

If people cannot save regularily then at least have the money automatically deducted out of your account to a savings account. At least you get to keep the money.

@FFB

Agreed. Keep the money in your control.

@Miranda

The “government coffers” is never a good place to kee you money. Thanks for a great comment.

@Amy

You’re one of the few – people who actually get money during tax season. Keep being responsible with the refund check and it will be worth it in the future.

@Kita

It’s certianly not a bad idea to be within your “comfort zone”. Unfortunately, many people have an irrational fear of underpaying. An educated decision alwasy trumps a fear based choice.

@David

Theoretically you are right – live on less and do something responsible with the refund. However, most people blow the refund. If you can manage your refund and resist your impulses to waste it then keep it up. You could try changing it and if you find you’re not managing it well then change it back. It really is a simply process to change your withholding.

@D

Fear is not bad. In fact, fear can be good. Irrational fear does need to be addressed. If you make the same as the year before and your family situation is the same, why would you own any more?

Be humble, think rationally, and ultimatley if it is a big issue in your marriage get the big refund. There are a lot worse things a spouse could do.

Craig, another post I disagree with you on! Most people can’t save, that’s why a tax refund is good.

Financial Samurai´s last post ..Someone Always Farts In A Crowd

@Financial Samurai

So if someone can’t save the only question is blow a little bit every month or blow a lot at the end of the year. Either way I guess they lose.

Nope. It’s MUCH easier to blow it every month on junk than it is to blow 1 year’s worth of your money when you get your refund. There is a greater chance that when people get their tax refund, they contemplate on how long it took to accumulate and may actually use it more wisely. They may still blow it away, but sometimes people stop to think what good they can do with their finances with a typical $2,400 refund.

$200/month… forget about it. It’s a rounding error for most people, and one meal and night out of town wipes out half of it just like that.

You can read my short Cookie argument here.

Financial Samurai´s last post ..Tax Refunds Are Good For Most People, Because Most People Can’t Save

I think it really depends on the person. But I’ve heard plenty of people talk about how they are using their refund to pay for X-mas or to fund a vacation or upgrade furniture. I think many people look at a refund as free money and don’t generally consider how to best save it.

FFB´s last post ..The Government Thanks You For Your Taxes

Craig, now I know why Iike you; you’re anothr pizza fan!

I used to be of the mindset that a large tax refund was a good thing and “found money”. A few years ago it became clear to me I wasn’t in a position to loan money to the government and made adjustments.

Last year we came out about even (underpaid ~$100 on federal and overpaid ~ $150 on state).

Bucksome´s last post ..Do Baby Boomers Know How to Find A Job?

I get a big refund every year, sometimes $4,000 to $6,000.

Am I a poor planner? No.

Am I missing out on interest? Not really.

I have a wife and three kids and I claim 10 dependents. I itemize.

Why the big refund? I have huge medical expenses that vary from year to year. One year they may be $10,000, the next they may be $30,000 (yes these are out of pocket expenses for a child with an autoimmune disorder). I can’t plan when she will be in the hospital.

I think most people who get a refund do so out of fear of the IRS rather than just about anything else. Taxes are highly confusing and complicated. Getting a refund (in the mind of most people) insures that they won’t get blindsided by a tax bill that they can’t pay. They simply err on the side of caution.

I really like your reply…I think this applies to most people I know, especially those who are considered “Middle class”. Not that the other views are wrong, it just depends on the person and how they plan their life.

Craig, I think you raise excellent points – and if we really saw that we’re giving Uncle Sam an interest free loan we’d realize our mistake and fix it – but I do have to agree with Samurai too – unfortunately most people can’t discipline themselves to save the money freed up from paying taxes.

That doesn’t mean they shouldn’t try. I would encourage folks to open an account and fund it with an automatic bank authorization as soon as they adjust their withholding on their check so that the money doesn’t “slip away”.

Jason @ Redeeming Riches´s last post ..5 Common Misconceptions About Life Insurance

I completely agree with your assessment from a financial standpoint. Giving the government the money is like giving them a free loan. That point is not something that can be argued… it’s just fact.

However, I don’t agree with some of your other assumptions. I get a humungous return every year. My wife and I are the type that spend when comfortable and don’t when uncomfortable. So… the big refund check at the end of the year goes directly into savings whereas the money every month would probably go… to the local pizza shop.

I realize I could set up a savings account and make interest on the savings. But, I’m not likely to do that monthly.

In the end, I like the idea of getting a fat sum (of my money) at the end of the year to put into savings. It’s forced savings in my world. We don’t go out and spend it on something frivolous… it goes right to our “rainy day” fund.

We adjusted our withholding for tax year 2009, and after estimating, it still appears that we’ll come away with some type of refund. I guess we’ll make similar changes for 2010, and do a little more math this time! And with our credit union giving us 4% for anything under $25,000, we lost out on about $16 in interest in 2009.

Andrew @ Earn Give Save´s last post ..Ask the Readers: What would you like to see here?

Like Amy and Ron we receive a refund mainly because of our three children. So, we receive what little federal taxes we do pay and then some. We then turn around and pay most of this to our state. Funny that the federal government apparently thinks we’re barely out of the poverty level, but our state thinks we’re loaded.

Alison@This Wasn’t In The Plan´s last post ..The Benefits of Banking Online

I agree to a point. I think if you have a plan for your refund it can be a great thing. For example, I’m using mine as a huge extra debt repayment.

In future years, who knows my priorities may be different. The point is, making a plan for every dollar, even your refund money, and sticking to it. Using your refund money for fun stuff like vacations is perfectly fine as long as its thought out beforehand and not done on impulse.

@d #7

If you work, you can adjust your withholding at work so less taxes are taken out. You don’t have to wait on your spouse to do so. But an even better idea is to send more money to retirement.

@All. Sorry. I’ve been in lala land while this great conversation was happening. I’m glad to see this generated some good comments.

@FS. If someone can be more responsible with a chuck of money instead of pieces of money then I recant. However, I’m still doubtful that is true. How much would it cost to do a nation wide survey and study people’s spending habits. Perhaps with a few hundred thousand dollars we could settle this think once and for all :).

@FFB. We must have the same type of friends because that is exactly the kind of stuff I hear people talking about doing with their tax returns.

@Bucksome Our bread maker just died after 10 years of use. There are no bread makers where we live overseas so we might just re-think our stance on homemade pizza.

You’re right that it is loaning money to the government.

@Ron

I completely understand your concern and I’m not sure that I would do any different. However, I’m not sure when you say you’re not really missing out on interest. I’m assuming your saying it is not much, but you are missing out on interest. If, however, that small amount of interest brings you a sense of financial peace then by all means talk the peace and forget the small interest payments.

@Jason

I know I raise excellent points (ha, ha). I completely agree that most people have trouble saving money freed up from paying taxes. To me that is a savings issue not a tax return issue. If you can’t save then either way I think this is a pointless discussion. Essentially the only question is blow it now or blow it then.

If, however, someone does save more one way or another then please don’t let me stop you from doing what works.

@Eric

Glad to hear that you are responsible with your returns. I think your probably the exception. If it’s helping you accomplish your financial goals then keep it up.

@Andrew

With low interest rates we are not talking about huge sums of money, your right.

@Alison

Having kids does always help you get a better tax rate. Sorry about the high state taxes.

@Ryan

I agree with me to a point too. Right on – though out beforehand and not done on impulse. If we could spend our money in this way everything would work out fine.

@laura

Correct. No matter how big your family is you can always adjust your withholding.

Craig Ford´s last post ..The Infinite Advantages Of Paying Cash For A New Car

I think that saying in general,” the idea of getting a free loan back is a financial disaster”, is not proper. Even though there may be rules to the game of finances everyone’s situation calls different measures. To the person who knows that they are not great at saving money this concept works great and to the person who has better discipline and budgeting habits it is not. It all depends on your plan. With that money not being available it forces a person to live off of less which should help them to not overstep their means and if they plan accordingly, they can use the refund to start an investment, create an emergency fund and boost their savings account for more comfortable living within that year. A person who is able to do that by pulling money from each check can achieve the same goals, yet larger amounts of money at one time can allow for better options when investing and saving.

Hi Craig,

While your post makes sense for most people, one major thing you are leaving out is the impact of the Earned Income Credit and Additional Child Tax Credit, which are both “refundable” tax credits that can generate tax refunds in and of themselves, regardless of the taxpayer’s withholdings. With the maximum Earned Income Credit at $5,751 for tax year 2011, and the Additional Child Tax Credit worth up to $1,000 per child, there are millions of people who receive humongous tax refunds of $4,000-$7,000 without putting in any tax withholdings during the year t all, it is just purely a payment of these refundable tax credits. I am not saying this is right or wrong or being in any way political, just mentioning why many people are ecstatic to get a refund at tax time and it has nothing to do with getting their own money back, it has to do with receiving the Earned Income Credit and Additional Child Tax Credit. FYI. Cool post all the same!

Perhaps the root of the disagreements above lie with the tax system itself?

For decades, my spouse and I have requested more withholding be taken from our income as an insurance against owing at the end of the year no matter what has transpired. The IRS refund resulting from this method is always used to pay off existing credit card or loan debt, considering any interest paid as expected expense. For the first time, Uncle has kept our $5000+ refund without refunding it, without explanation other than that given thousands of other Americans this year. The $5000+ has not been deposited to our bank, at present 7 months late, nor has any communication from IRS suggesting when it may be “refunded”. Worse, now that we are half thru the next year, withholding for this year is also being kept by IRS at a higher than earned rate, so after the year’s end we should be owed double this year’s $5000+ from IRS as a “refund”. No commlunication and definitely no refund of moneys already paid to Uncle.

hmmmmmm This is also the first time period that govt. Stimulus Checks were sent out! Were those “gifts of stimulus” paid from our income tax, so the gov has actually SPENT our over paid income tax “refund” ??? and those funds are NEVER going to be refunded to us?