A while ago I wrote a post talking about how to save for college education costs using a 529 account, a Roth IRA or an ESA. Of those account types one of my favorites is the 529.

529 plans are a great deal because they offer a way to save money for your child’s education in a way that shields it from federal taxes. Not only are the savings tax free as long as they’re used for education purposes for your child, but in some states you can also receive a deduction on your taxes for contributing to a 529. The plans have gained a lot of popularity over the past decade.

In 2001, 529 plans held just $13.6 billion in assets, according to data from the College Savings Plans Network. Through the first quarter of 2014, that amount had increased to $210.6 billion.

A lot of people are seeing the benefits of opening a 529 for their children. So what are the basic rules for a 529 plan, and how do you know what 529 plan is the best for you to invest in when there are so many available? Can you still get tax breaks if you invest in a plan outside of your home state?

Let’s start by looking at 529 plans, what they are and what the benefits are.

What Is A 529 Plan?

The 529 plan is named after section 529 of the Internal Revenue Code, and these types of savings plans were started back in 1996. The plans are usually operated by a state or educational institution, and are typically of two types.

- 529 College Savings Plans: These plans are much like a typical retirement account where you put your funds in and are able to choose from certain investments that are made available via the plan. Your savings can increase or decrease depending on how your investments do.

- 529 Prepaid Plans: These types of 529 plans allow you to pre-pay part or all of the cost of an in-state public college education. By doing this you’re able to pay for education at today’s rates, and avoid paying inflated costs.

Typically I would recommend using the 529 college savings plan mainly because they’re more flexible. They can be used at any school of your choosing in any state (for the most part), whereas with the prepaid plans you may be tied into a specific state or school, or forfeit some of the savings you would have enjoyed if you end up going to school out of state.

529 Contribution Limits

When contributing to a 529, the plan and state you’re investing in may have it’s own limits as far as how much you can contribute, and it can vary pretty substantially. Make sure to check the plans you’re thinking of investing in before signing up.

For federal tax purposes, your contributions are limited only by the gift tax exclusion, which says that you can give a gift of up to$14,000 for 2014, or $28,000 for couples without having to worry about gift tax implications.

When giving to a 529, however, you can front load up to 5 years of gift tax exclusions, so hypothetically you could put in up to $70,000 right away without having gift tax implications – and that money could grow tax free for that child’s education right away.

Things To Look For In A 529 Plan

When considering what 529 plan to sign up for, there are a few main things to consider:

- Does your state have a tax deduction? Some states will offer a state tax deduction for contributing to their state’s plan. Others will offer a deduction, even if contributions are made to another state’s plan. Look your state up here to find out what your state offers. If it does offer a deduction, you may want to consider your state’s plan.

- What are the fees? One thing that can hamper your investment performance is signing up for a 529 plan that has higher than average fees. Make sure your plan has low or reasonable fees for what investment options you’re getting.

- Good investment options? 529 plans don’t all have the same investment options, so make sure you’re getting good investment options like index funds and/or ETFs in the plan.

- Good management? Make sure that the 529 plan is managed well by doing your research beforehand.

The Best 529 College Savings Plans

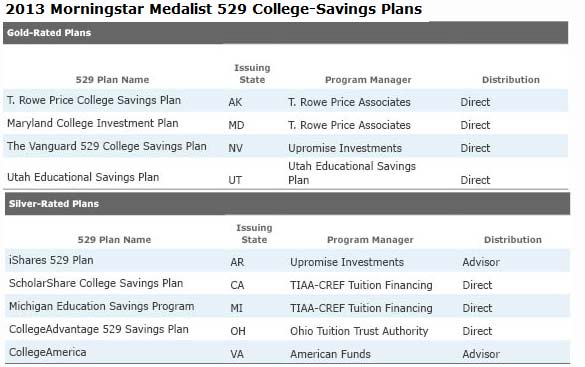

So how do you even start trying to figure out what plans out there are the best? Thankfully the research has already been done for us. For example, a few months ago Morningstar put out their complete list of the best 529 college savings plans for 2013. From that list I’m going to list the top eight 529 plans on their list. They were all given either their gold or silver medal rating. What does a gold or silver medal signify?

Morningstar’s analysts have identified nine 529 college-savings plans as the nation’s best, awarding them Gold and Silver Morningstar Analyst Ratings for 2013. These top medals signal that Morningstar has the highest conviction in the plans’ ability to serve college savers well over the long term. In 2012, eight plans were awarded Gold and Silver Morningstar Analyst Ratings, which are forward-looking, qualitative ratings issued annually.

Here are the best 529 college savings plans for 2013:

The best plans available according to Morningstar haven’t changed much from 2012. Only one plan was added to the best gold and silver plans, the California 529 plan. Here’s the list:

- Gold – Utah’s Utah Educational Savings Plan offers great passive investments from Vanguard, my favorite mutual fund company. When we start our son’s 529, we’ll be using this one since our state has no tax deduction.

- Gold – The Vanguard 529 College Savings Plan of Nevada also offers Vanguard’s great low cost passive investments.

- Gold – Alaska’s T. Rowe Price College Savings Plan offers investments from T. Rowe Price and has been rated by Morningstar as industry leaders for their active investing strategies and reasonable cost.

- Gold – Maryland’s Maryland College Investment Plan also offers investments from T. Rowe Price, very similar to the plan above.

- Silver – Arkansas’ iShares 529 Plan offers a low cost ETF based investing option.

- Silver – Michigan Education Savings Program offers mostly indexed options run by TIAA-CREF, and historically have had low fees.

- Silver – CollegeAdvantage 529 Savings Plan of Ohio has a nice variety of investing options to consider, all at a reasonable cost.

- Silver – Virginia’s College America plan is managed by American funds, and is the country’s largest at $33 billion in assets. Offers age based options for investing, and offers low fees.

- Silver – ScholarShare College Savings Plan of California is the newest addition to the bunch, run by TIAA-CREF.

Here are the best 529 college savings plans for 2012:

- Gold – Utah’s Utah Educational Savings Plan

- Gold – The Vanguard 529 College Savings Plan

- Gold – Alaska’s T. Rowe Price College Savings Plan

- Gold – Maryland’s Maryland College Investment Plan

- Silver – Virginia’s College America

- Silver – Arkansas’ iShares 529 Plan

- Silver – CollegeAdvantage 529 Savings Plan of Ohio

- Silver – Michigan Education Savings Program

Read up on the rest of Morningstar’s 529 plan ratings here.

Are you already investing in a 529 plan, and if so, which one? Are you getting a state tax deduction?

When my son was born in 8/2011 we set up a 529 with the Utah Plan. We are currently putting in $100/month, but I imagine that won’t be enough for a top rate school. When the time comes I’ll have to sit down and discuss his options. Who knows how colleges will operate in the future. Community colleges work out great for a lot of people, so that’s an option. All I know now is that college tuition is in a bubble phase with far too many students graduating with tens (sometimes hundreds) of thousands of dollars of debt. I don’t see how everyone can pay back what they owe. Eventually the market will have to correct this issue.

Agreed, the cost of college is quickly getting out of hand – it’s a bubble waiting to burst. When students are graduating with thousands in school debt and with no big job prospects, we’ve got a major issue.

I too just signed my daughter up on the Utah Educational Savings Plan. I am a relatively new dad, 19 month old daughter but I decided to start early because I hope when my daughter finishes school she will not be buried in debt. I linked the UESP with a GradSave college registry account which lets me share her profile with family and friends online and they gift directly to her 529. Its a win win, my family gives a gift that is meaningful and I worry that much less.

We are using the Ohio College Advantage Savings Plan, we have been the plan for three years and have been very pleased with it. Since we live in Ohio, we do get a tax deduction.

I know of at least one other blogger who has mentioned using the Ohio College Advantage Plan, I hear it’s a good one.

“When giving to a 529, however, you can front load up to 5 years of gift tax exclusions, so hypothetically you could put in up to $65,000 right away without having gift tax implications – and that money could grow tax free for that child’s education right away.”

Oh to be wealthy. If I had the cash I would totally load up 65k in these accounts for each child. Incredible tax savings.

This is really good info, thanks. I signed up with a registry called GradSave.com where my mom gives $50 per month for my kid, and we had a first birthday where we had friends and family gift to Jeff’s college savings fund. All in we got almost $1,000 in gifts for his first birthday. Gradsave helped me set up my 529 and the money now grows tax free. I really love and reccomend them. gradsave.com

For as boring as I invest in mine, the most important factor to me when choosing a 529 has been the state tax deduction. That’s a big upfront boost.

Good timing, I was going to open a 529 for my daughter next month. I was going to use USAA since I really like them and they always advertise that their 529 beats others, but now I see that they only have the best 10 year performance (not that great for 1 year or 5 year) and they charge an extra $15 a year if you are not a resident of Nevada.

The Utah plan is looking good, several choices for the age based plans (so it will adjust itself automatically based on my daughters age), and extra fees will be waived if I get quarterly statements online. Sounds like it will work well for us.