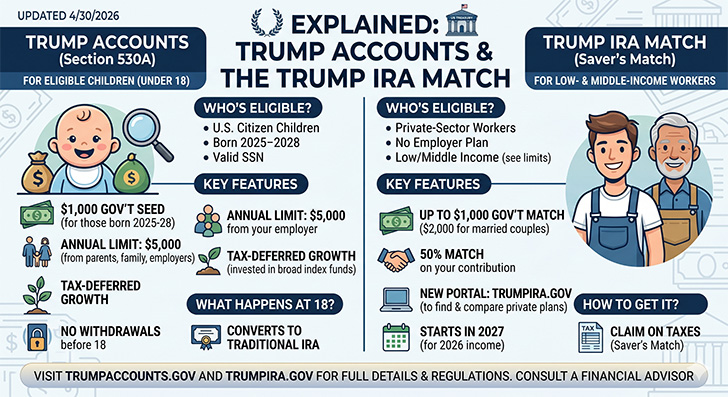

President Donald Trump signed an executive order on April 30, 2026, directing the Treasury Department to launch TrumpIRA.gov. This new online platform aims to expand retirement savings access for the tens of millions of American workers whose employers do not offer a 401(k) or similar plan.

This initiative builds on earlier efforts, including the Saver’s Match (from the 2022 Secure 2.0 Act), and focuses on practical, long-term wealth building—aligning with timeless principles from investors like Jack Bogle (low-cost indexing), Warren Buffett (patient, disciplined saving), and Benjamin Graham (focus on value and avoiding unnecessary risk). While not a brand-new account type in the traditional sense, it creates an easier pathway to existing IRAs and leverages government matching for eligible low-income savers.

Quick Navigation

Who Is Eligible for TrumpIRA.gov and Related Benefits?

- Primary users: Workers without employer-sponsored retirement plans (estimated at roughly 40% of full-time and 80% of part-time employees).

- Saver’s Match eligibility (starting in 2027): Lower-income individuals can receive up to $1,000 annual government match on contributions. For 2027, this generally applies to singles earning under about $35,500 or joint filers under $71,000 (exact thresholds may adjust with inflation or guidance). The match equals up to 50% of your contributions, deposited directly into your retirement account.

- Broader access: Any worker can use the site to compare and enroll in private-sector IRAs or similar plans. Future expansions could include automatic enrollment features or incentives for private donors to contribute.

The platform will function as a marketplace, letting users filter plans by fees, minimums, investment options, and more—promoting informed, low-cost choices over high-fee products.

How TrumpIRA Accounts Differ from Existing Retirement Options

TrumpIRA.gov does not invent a wholly new account structure but streamlines access to traditional or Roth IRAs (and potentially other plans) for underserved workers. Here’s a comparison:

- Vs. Traditional Employer 401(k): No employer match required (though some plans might offer one). Easier setup without workplace involvement. Contribution limits follow standard IRA rules (e.g., $7,000 for under 50 in recent years, plus catch-up for older savers—check current IRS limits).

- Vs. Standard IRA: The key difference is the facilitated enrollment and awareness via TrumpIRA.gov, plus the Saver’s Match boost for qualifying low earners. No earned income requirement changes, but the site lowers barriers for gig workers, part-timers, and small-business employees.

- Vs. Child “Trump Accounts” (Separate Program): Note that “Trump Accounts” (under the 2025 One Big Beautiful Bill Act) are distinct custodial IRAs for minors under 18, with a $1,000 federal seed for births 2025–2028, up to $5,000 annual contributions, and strict investment rules (e.g., low-cost U.S. index funds). These launched contributions on July 4, 2026, and convert to standard IRAs at age 18. The April 30 announcement focuses on adult workers.

Tax treatment mirrors standard IRAs: Traditional for upfront deductions (if eligible) and tax-deferred growth; Roth for tax-free qualified withdrawals. Withdrawals before 59½ generally face penalties, encouraging long-term holding.

Key Features and Practical Details

- Launch timeline: Website development underway, with full Saver’s Match integration targeted for 2027.

- Investment approach: Users select private-sector plans, ideally emphasizing low-cost index funds or broad-market ETFs—consistent with Bogle’s “don’t look for the needle in the haystack, just buy the haystack” philosophy and Malkiel’s random-walk efficient market insights. Avoid high-fee or speculative options to maximize compounding.

- Government role: Treasury handles the platform and match. Private donors may contribute in the future per guidance.

- How to get started (expected): Visit TrumpIRA.gov once live, compare plans, open an account, contribute (via payroll if possible or direct), and claim the match if eligible through tax filing or direct deposit.

Why This Matters: Long-Term Investing Perspective

Retirement security remains a challenge for many. With roughly half of private-sector workers lacking easy access to plans, this addresses a real gap without overcomplicating the system.

From a common-sense viewpoint:

- Start early and consistent: Even modest contributions (boosted by the match) harness compound growth over decades.

- Keep costs low: Prioritize plans with expense ratios under 0.1% where possible.

- Diversify broadly: U.S. total market or S&P 500 index funds have historically delivered strong long-term returns with manageable volatility.

- Pair with faith and discipline: As stewards of resources, consistent saving reflects wisdom (Proverbs 21:20) while avoiding debt traps or get-rich-quick schemes.

This isn’t revolutionary like a new Roth variant, but it’s pragmatic—leveraging existing infrastructure, public-private partnerships, and incentives to help more families build wealth. It complements child Trump Accounts for multi-generational planning.

Action Steps for Readers

- Check your employer plan status.

- Monitor TrumpIRA.gov for launch details and guidance.

- If eligible for Saver’s Match, plan contributions to maximize the $1,000 potential.

- Consult a tax advisor or fiduciary for personalized fit with your overall portfolio.

- Consider combining with other vehicles (529s for kids, HSAs for health) for a holistic strategy.

As Burton Malkiel and others remind us, investing success comes from time in the market, not timing the market. Tools like TrumpIRA.gov make participation simpler for more Americans. Stay informed, invest steadily, and focus on the long game—your future self (and family) will thank you.

This article is for informational purposes. Tax laws and program details can change; verify with IRS.gov or a professional.

Share Your Thoughts: