I‘ve always believed that the best way to build wealth over time is through simple, steady strategies that minimize risk and let the market do the heavy lifting. As someone who’s risk-averse by nature, I lean heavily on index investing—it’s like the tortoise in that old fable, slow and steady, but it wins the race. Drawing from wisdom shared by legends like Jack Bogle, the founder of Vanguard, and Warren Buffett, who once said most people should just buy an S&P 500 index fund and hold it forever, index investing has transformed how everyday Americans approach long-term investing and retirement planning.

In this article, we’ll dive into the history of index funds, explore the solid research that backs them up, meet some of the key proponents who’ve championed this approach, see how it’s being used today, and even break down practical strategies like the three-fund portfolio. If you’re in the United States and looking to secure your financial future without chasing hot stocks or paying high fees, this is for you. Let’s get started.

Quick Navigation

A Brief History of Mutual Funds: The Foundation for Modern Investing

Before index funds changed the game for everyday investors like you and me, mutual funds laid the groundwork for pooled investing, making it possible for ordinary folks to dip their toes into the stock market without needing a fortune or a Wall Street insider.

The roots of mutual funds stretch back to the 18th century in the Netherlands, where a Dutch merchant named Adriaan van Ketwich created the first investment trust in 1774, called Eendragt Maakt Magt—essentially a way for small investors to pool their money and spread risks across global ventures like plantations and loans. This idea crossed the Atlantic, influencing early American versions.

In the US, the concept took off in the 1920s amid a booming economy. The Massachusetts Investors Trust, launched in 1924, became the first open-end mutual fund, allowing investors to buy and redeem shares at net asset value anytime. It was a hit because it democratized investing— no more closed-end trusts with fixed shares that traded like stocks. As someone who’s all about low-risk, long-term strategies, I appreciate how this shifted power to the investor, echoing Jack Bogle’s later emphasis on simplicity and low costs.

Mutual funds exploded in popularity through the mid-20th century, but they weren’t without bumps. The 1929 stock market crash exposed flaws in some leveraged funds, leading to the Investment Company Act of 1940, which brought much-needed regulations for transparency and fairness. By the 1950s and 1960s, funds focused on active management, with managers picking stocks to beat the market—a far cry from the passive approach I favor today. Yet, this era set the stage for innovation.

As research from economists like Eugene Fama and Paul Samuelson highlighted market efficiency, it became clear that active funds often underperformed after fees. This paved the way for index funds in the 1970s, pioneered by Bogle at Vanguard. From humble Dutch beginnings to trillions in assets now, mutual funds have evolved into a cornerstone of retirement planning, reminding us of Proverbs 13:11: “Wealth gained hastily will dwindle, but whoever gathers little by little will increase it.” For risk-averse investors, they’re a tool for steady growth when chosen wisely—preferably the low-cost index variety.

The Origins: How Index Investing Got Its Start

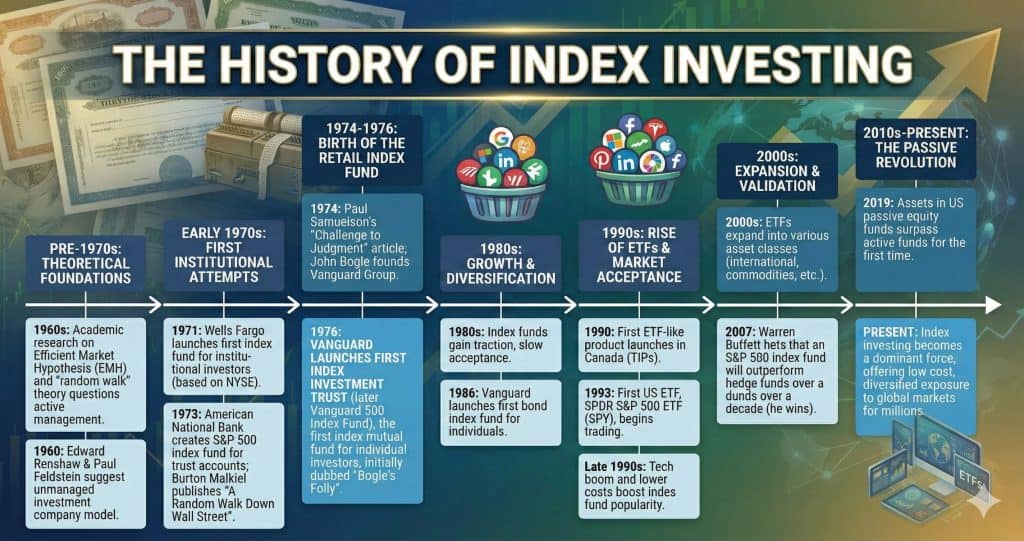

Index investing didn’t just appear out of nowhere—it was born from a mix of academic ideas and practical innovation during a time when Wall Street was all about active stock-picking. The concept can trace its roots back to the 1960s.

In 1960, researchers Edward Renshaw and Paul Feldstein proposed the idea of an “unmanaged investment company” in a paper, suggesting that a fund could simply mirror the market instead of trying to beat it. This was revolutionary because, up until then, investing meant relying on fund managers to pick winners.

But it wasn’t until the early 1970s that the first real index fund came to life. In 1971, Wells Fargo created the first index fund for institutional investors, aiming to track the performance of the New York Stock Exchange. It was a modest start, mostly for big pension funds, and it faced skepticism from those who thought passive investing was too boring or ineffective.

Then came the game-changer. John “Jack” Bogle, after being fired from his job at Wellington Management, founded Vanguard in 1975 with a mission to put investors first. In 1976, he launched the First Index Investment Trust, which later became the Vanguard 500 Index Fund. This was the first index fund available to everyday retail investors in the US. At launch, it only raised $11 million—far short of its goal—but Bogle persisted. He believed in low costs and broad diversification, principles that align perfectly with a risk-averse mindset.

Over the years, index funds evolved. By the 1980s and 1990s, more funds emerged tracking various indices like the Dow Jones or international markets. The introduction of exchange-traded funds (ETFs) in the 1990s, starting with the SPDR S&P 500 ETF in 1993, made index investing even more accessible and liquid. Today, index funds hold trillions in assets, proving that humble beginnings can lead to massive success.

The Research That Proves Why Index Investing Works

What makes index investing so appealing isn’t just its simplicity—it’s the mountain of evidence showing it outperforms active strategies for most people over the long haul. At the heart of this is the Efficient Market Hypothesis (EMH), developed by economist Eugene Fama in the 1960s. EMH suggests that stock prices reflect all available information, making it nearly impossible for active managers to consistently beat the market after fees.

Study after study backs this up. For instance, research from S&P Dow Jones Indices shows that over 15-year periods, about 92% of active large-cap fund managers underperform the S&P 500. Why? High fees eat into returns, and even skilled managers can’t predict the market reliably. Burton Malkiel, in his classic book “A Random Walk Down Wall Street,” argues that stock movements are largely random, so trying to time or pick them is like gambling.

Paul Samuelson, a Nobel laureate, was an early advocate, writing in 1974 that most portfolio managers should go out of business because they couldn’t beat a simple index. And Benjamin Graham, the father of value investing and mentor to Warren Buffett, admitted late in life that a low-cost index fund was the best choice for most investors.

From a risk-averse perspective, index funds offer diversification across hundreds or thousands of stocks, reducing the impact of any single company’s failure. They’re also tax-efficient, with lower turnover meaning fewer capital gains distributions. In short, the data doesn’t lie: for long-term investing in retirement accounts like 401(k)s or IRAs, index funds provide reliable growth without the stress of constant monitoring.

Popular Proponents Who Championed Index Investing

No discussion of index investing would be complete without highlighting the voices that made it mainstream. Jack Bogle stands out as the pioneer. His philosophy at Vanguard was “don’t look for the needle in the haystack—just buy the haystack.” He emphasized low fees, noting that even a 1% annual fee can eat up 30% of your returns over 40 years.

Warren Buffett, the Oracle of Omaha, might be known for active investing, but he repeatedly recommends index funds for average folks. In his 2013 Berkshire Hathaway letter, he instructed that his wife’s inheritance go into a low-cost S&P 500 index fund. Buffett’s bet against hedge funds in 2008, where an index fund outperformed them handily over a decade, further proved his point.

Burton Malkiel and Paul Samuelson, as mentioned, provided the academic backbone. Even Benjamin Graham, in a 1976 interview, said he’d advise most people to use index funds. These experts aren’t just theorists; their advice has helped millions build wealth steadily.

On a personal note, as someone who values prudence and planning ahead, this approach resonates. As it says in Proverbs 21:5: “The plans of the diligent lead to profit as surely as haste leads to poverty.” Index investing encourages diligence over get-rich-quick schemes.

How Index Investing Is Used Today

Fast forward to now, and index investing is everywhere. In the US, passive funds now hold more assets than active ones, with over $13 trillion in index mutual funds and ETFs as of recent data. They’re a staple in retirement planning, often the default option in 401(k) plans from employers like those in tech or manufacturing.

Investors use them for everything from college savings in 529 plans to building emergency funds in taxable accounts. The rise of robo-advisors like Betterment or Wealthfront has made it even easier, automatically allocating to index funds based on your risk tolerance.

With inflation and market volatility, index funds shine by capturing broad market returns without trying to outsmart the crowd. For long-term investors, this means compounding growth—think 7-10% average annual returns historically for stock indices, adjusted for inflation.

Building a Simple 3-Fund Portfolio with Index Funds

One of the most straightforward ways to implement index investing is the three-fund portfolio, popularized by the Bogleheads community. It’s elegant in its simplicity: just three low-cost index funds covering the major asset classes.

- Total US Stock Market Index Fund: This captures the entire US equity market, like Vanguard’s VTSAX or Fidelity’s FSKAX. It includes large, mid, and small-cap stocks for broad exposure.

- Total International Stock Market Index Fund: For global diversification, something like VXUS from Vanguard or IXUS from iShares. It helps hedge against US-only risks.

- Total Bond Market Index Fund: For stability, BND or similar tracks US investment-grade bonds, reducing volatility.

Allocations depend on your age and risk tolerance. A 30-year-old might go 60% US stocks, 30% international, 10% bonds. As you near retirement, shift more to bonds. This setup keeps costs under 0.1% annually and rebalances easily once a year.

It’s a set-it-and-forget-it strategy, perfect for busy families or those saving for retirement.

Low-Cost Places to Invest in Index Funds in the US

Getting started is easier than ever with brokerages offering commission-free trading. Vanguard leads the pack with its investor-owned structure and rock-bottom fees—think 0.04% for many funds.

Fidelity is another top choice, with zero-expense-ratio index funds like FZROX for total market exposure. Charles Schwab offers similar low-cost options, and their SCHB ETF is a favorite.

For ETFs, BlackRock’s iShares line provides flexibility. Open a brokerage account, link your bank, and buy shares. If you’re in a 401(k), check for target-date funds built on indexes.

Remember, the key is low costs—avoid funds with loads or high expense ratios.

Low Cost Index Fund Providers

Here’s a breakdown of some of my favorite low-cost providers for index investing in the US, perfect for everyday folks aiming for steady growth without the gamble of active management. (In case you’re wondering, I use Vanguard!)

- Vanguard

- Type: Brokerage

- Key Low-Cost Index Funds/ETFs: VTSAX (Total Stock Market), VOO (S&P 500 ETF), VFIAX (500 Index)

- Average Expense Ratio: 0.03%-0.04%

- Management Fee: None (self-directed)

- Minimum Investment: $0 for ETFs; $3,000 for Admiral shares

- Best For: Risk-averse investors seeking broad diversification and the original low-cost pioneer, as Bogle intended.

- Fidelity

- Type: Brokerage

- Key Low-Cost Index Funds/ETFs: FZROX (ZERO Total Market), FNILX (ZERO Large Cap), FXAIX (500 Index)

- Average Expense Ratio: 0%-0.015%

- Management Fee: None (self-directed)

- Minimum Investment: $0

- Best For: Beginners who want zero-fee options and easy access to tax-advantaged accounts like Roth IRAs.

- Charles Schwab

- Type: Brokerage

- Key Low-Cost Index Funds/ETFs: SWTSX (Total Stock Market), SWPPX (S&P 500), SCHB (Broad Market ETF)

- Average Expense Ratio: 0.02%-0.03%

- Management Fee: None (self-directed)

- Minimum Investment: $0

- Best For: Cost-conscious folks building a three-fund portfolio with commission-free trading.

- Betterment

- Type: Robo-Advisor

- Key Low-Cost Index Funds/ETFs: Uses ETFs like VTI (Vanguard Total Stock), BND (Bond) in automated portfolios

- Average Expense Ratio: 0.07%-0.13% (ETF avg)

- Management Fee: 0.25%

- Minimum Investment: $0

- Best For: Hands-off investors who prefer automated rebalancing, aligning with prudent, set-it-and-forget-it strategies.

- Wealthfront

- Type: Robo-Advisor

- Key Low-Cost Index Funds/ETFs: Uses ETFs like VTI, VEU (International), BND in diversified portfolios

- Average Expense Ratio: 0.06%-0.13% (ETF avg)

- Management Fee: 0.25%

- Minimum Investment: $500

- Best For: Tech-savvy savers focused on tax-loss harvesting and long-term growth without daily oversight.

As Warren Buffett often says, the secret to investing is to figure out the value of something and then pay a fair price—low fees ensure you’re not overpaying. Start with what fits your risk tolerance, perhaps a simple three-fund setup, and let time do the rest.

Wrapping It Up: Why Index Investing Stands the Test of Time

From its academic origins to today’s dominance, index investing has proven itself as a reliable path to long-term wealth. As a risk-averse investor inspired by Bogle and Buffett, I see it as the smart, common-sense choice for most Americans. Start small, stay consistent, and let time work its magic.

If you’re ready to dive in, consult a fiduciary advisor or use free tools from these brokerages. Your future self will thank you.

FAQ Section

- What is the history behind the first index fund? The first index fund was created by Wells Fargo in 1971 for institutions, but Jack Bogle’s Vanguard 500 in 1976 made it accessible to retail investors.

- Why do index funds outperform active funds? Research like the Efficient Market Hypothesis shows markets are hard to beat consistently. High fees in active funds erode returns, with 92% underperforming over 15 years.

- Who are the main proponents of index investing? Key figures include Jack Bogle, Warren Buffett, Burton Malkiel, Paul Samuelson, and Benjamin Graham.

- How can I start a three-fund portfolio? Choose low-cost funds for US stocks, international stocks, and bonds. Allocate based on your risk level and rebalance annually.

- Where are the best places to buy index funds? Vanguard, Fidelity, and Schwab offer the lowest costs and easy access for US investors.

- Is index investing suitable for retirement? Absolutely—it’s ideal for long-term growth in IRAs or 401(k)s due to diversification and low fees.

- What are the risks of index investing? Market downturns affect indexes, but over time, they recover. Diversification helps mitigate this.

{kind=link}

Share Your Thoughts: