If you’re like me, trying to juggle family finances while keeping an eye on long-term goals like retirement investing, you’ve probably felt the sting of rising health insurance costs.

Here in the US, premiums have been climbing steadily—reports from 2025 show average family coverage hitting around $26,000 a year, with some folks seeing spikes up to 26% in marketplace plans. That’s no small change, especially when you’re aiming to sock away more for retirement, or for important savings goals.

As our health insurance costs started going up exponentially, I started looking into health insurance alternatives a couple of years back. Traditional insurance felt like a black hole for my budget, sucking up more and more of our budget every year. That’s when I discovered health sharing ministries—community-based setups where members pool resources to cover medical needs.

After some prayerful consideration and a lot of research, I joined Impact Health Sharing one year and a few months ago. Today, I’m sharing my real-world review, including the benefits we’ve seen, the roadblocks we’ve run into, and how it fits into a faith-centered approach to money management.

Quick Navigation

The High Cost of Health Insurance: Why I Looked for Alternatives

Let’s start with the elephant in the room: why bother with something outside traditional health insurance? Well, in 2025, health care costs kept soaring due to factors like higher drug prices, especially for those trendy weight-loss meds, and fewer insurers in the market leading to less competition. According to sources like the American Academy of Actuaries, premiums rose because of increased demand for pricey treatments and overall inflation in medical services.

For my family of four, our old Health Partners insurance plan was costing us $1,182 a month in premiums, plus an annual family deductible of $10,200. That meant we could be on the hook for almost $24,384 out of pocket each year before insurance even kicked in—combining those premiums and the full deductible. That’s money I could’ve directed towards more important things. With health costs eating into savings, it was time for a change. Health sharing ministries appealed because they’re often 30-50% cheaper, and they align with biblical principles of bearing one another’s burdens, like in Galatians 6:2. No wonder more people are turning to them; membership in these groups has surged since the Affordable Care Act, with millions opting in for affordability and community support.

What Is a Health Sharing Ministry?

If you’re new to this, a health sharing ministry isn’t insurance—it’s a nonprofit arrangement where like-minded individuals contribute monthly shares to help cover each other’s eligible medical bills. These ministries have been around since the 1980s, evolving as a way to handle skyrocketing health costs without the bureaucracy of big insurers.

Unlike insurance, which is regulated and profit-driven, health sharing focuses on community and often incorporates faith elements, though not all require religious affiliation. Members agree to guidelines, like promoting healthy living, and funds are distributed based on needs. It’s exempt from ACA mandates, meaning no penalties for not having traditional coverage. Entities like Impact Health emphasize wellness and transparency, making it a solid health insurance alternative for those who are generally healthy and risk-averse like me.

History of Impact Health Sharing

Impact Health Sharing launched in 2020, founded by Phil and Angela Chrysler, a couple of faith-inspired entrepreneurs from the Midwest. They aimed to create a modern, tech-savvy health sharing option that prioritizes member wellness over profits. Starting small, they’ve grown to over 19,500 members by 2025, sharing more than $275 million in medical needs.

What sets Impact apart is its non-religious base—while faith plays a role in their community ethos, it’s open to anyone committed to healthy living. They’ve avoided rate hikes for five years running, which is huge in an era of inflating costs. From my research, their growth mirrors the broader health sharing movement, which traces back to Christian ministries in the ’80s but has expanded to secular options too. Impact’s story is one of innovation, using apps and quick payments to make sharing seamless.

How Health Sharing Works with Impact

Signing up was straightforward. You answer a few questions about your household—no deep dives into medical history upfront, though they do review pre-existing conditions case-by-case. For seniors over 65, there’s no exclusion, which is a relief for older folks.

Here’s the basics of how it operates:

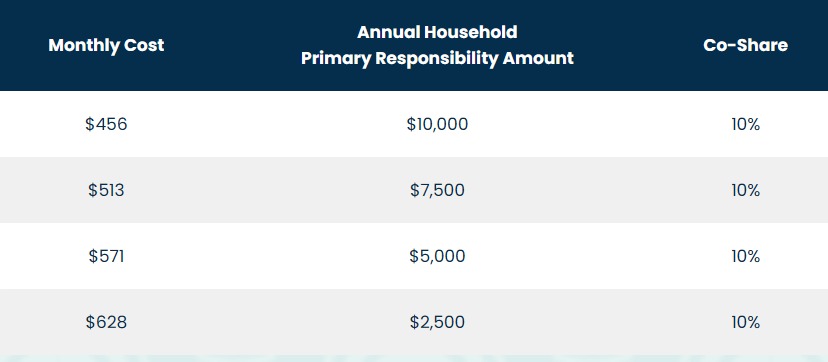

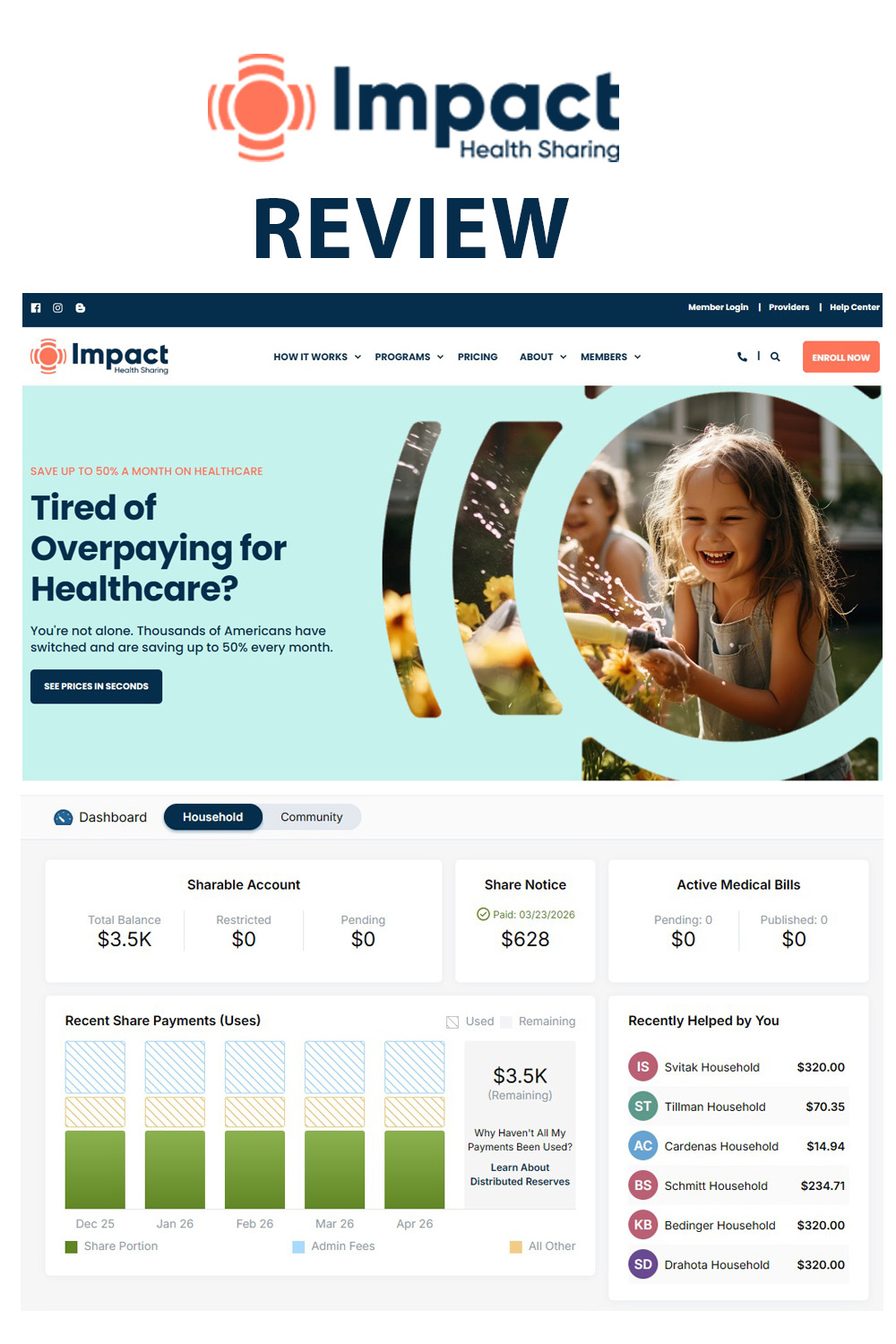

- Monthly Contributions: You pick a plan based on your personal responsibility amount (PRA), similar to a deductible. For my family of four, we chose a $2,500 PRA and pay $628 per month, which totals $7,536 annually.

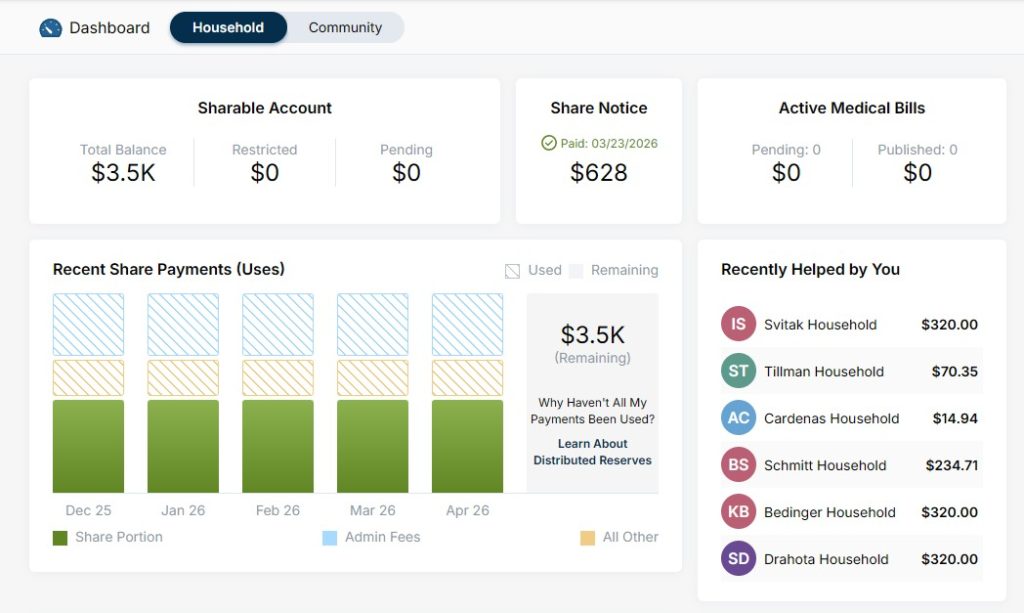

- Submitting Needs: If you have a medical bill you submit it via their app, or preferrably have the provider submit it directly. The community shares the cost once your cumulative costs are over your PRA, with bills often paid in under 15 days. After the PRA, there’s a 10% co-share that members pay on eligible expenses, which helps keep overall costs down for everyone.

- Perks Included: Unlimited telehealth (We’ve used it a few times for minor stuff, you just make an appointment and do a video call with a doctor), $0 generic prescriptions, dental and vision discounts, and even wellness rewards (which can save you up to $150/month on your PRA). I earned $150 last month by logging our online supplement purchases, which reduces my PRA.

- No Networks: Freedom to choose any doctor, which was key for me—I didn’t want to switch our family physician in the Twin Cities area.

It’s all handled through a secure platform, and transparency is big; you see where shares go. I appreciate how this cuts out middlemen, potentially saving 50% monthly. Our out-of-pocket maximum sits at around $10,036 per year (the monthly fees plus the $2,500 PRA), not counting the 10% co-share on amounts beyond that, which feels more manageable than our old setup.

Pros and Cons of Health Sharing

No option is perfect, especially for someone risk-averse like me. Let’s break it down.

Pros:

- Cost Savings: I’ve saved over $6,600 in premiums alone this past year compared to our old Health Partners plan, not to mention the lower deductible. That extra cash went straight into maxing my Roth IRA, buying low-cost index funds for long-term growth.

- Community Feel: It’s rewarding knowing my shares help others, aligning with faith values. Impact’s members are wellness-focused, which keeps costs down.

- Flexibility: Quick payouts, and extras like free annual checkups (up to $150 in labs covered).

- Wellness Incentives: Rewards for healthy habits encourage better living, which reduces future risks.

- Prescriptions: $0 Generic Medication Program when you select a 30 or 60-day supply.

Cons:

- Not Insurance: There’s no guarantee of coverage; if the ministry faces issues, you’re at risk. Though Impact has a strong track record, I keep an emergency fund beefy just in case.

- Pre-existing conditions: One problem we ran into this year were having bills denied due to pre-existing condition exclusions for my wife. We ended up having to spend a bunch of time having providers re-categorize our bills to avoid these exclusions because sometimes even a cursory mention of a pre-existing condition on an unrelated appointment would exclude the whole visit.

- Limited Coverage: Things like maternity (after waiting periods) or certain pre-existing conditions might not be fully shared. I double-checked my family’s health before joining. Also, the 10% co-share after the PRA can add up, but thankfully it maxes out at $5,000 per household per year.

- Provider Acceptance: Some doctors hesitate with sharing plans, but if they refuse to submit to Impact, you can submit a bill directly yourself on their website. We had to do this a couple of times when a practice refused to bill Impact.

- Regulatory Gaps: Unlike insurance, it’s not protected by state guarantees, so if you’re high-risk, you might want to stick with traditional plans.

Overall, for healthy families, the pros outweigh the cons, but do your due diligence.

Example Costs of Impact Health Sharing

Costs vary by age, family size, and PRA. For a single adult in their 30s, plans start at $73/month. My family of four pays $628/month for a $2,500 PRA—far less than the $1,182 we’d pay elsewhere, and our potential out-of-pocket max is $10,036 annually before the 10% co-share. Here’s an example of what costs look like for a family of 4 in my case:

Here’s a breakdown of average costs based on your family size:

- Individual: $73-$200/month

- Couple: $150-$400/month

- Family: $378-$800/month (our $628 fits in here for the lower PRA option)

- Seniors with Medicare: Around $100/month supplemental.

Add wellness rewards, and you can shave off more. In our case by claiming our $150 monthly supplement purchases at Amazon for their wellness rewards benefit we saved almost $1800 off of our PRA. That means we only had to have $700 in medical costs to reach our deductible/PRA. That was huge!

Compared to 2025’s average premium of $16,000 per employee for employer plans, it’s a steal. In our case, switching dropped our annual exposure from nearly $24,384 (old premiums plus deductible) to about $10,036 plus co-share, freeing up funds for smarter money moves.

My One-Year Review: The Good, the Bad, and the Faithful

After 12 months, I’m mostly pleased. We had a few doctor visits and one ER trip for my kid’s sprained ankle. Most bills were submitted by the doctor’s offices directly, although we did have to submit a few manually through Impact’s site.

Shares covered everything above our $2,500 PRA, though we also chipped in the 10% co-share over the PRA. Telehealth saved us time and money on a flu scare.

The bad? We had some issues getting doctor’s offices to bill Impact direct, and had to spend more time than we would have liked when several of my wife’s bills were denied initially due to pre-existing condition exclusions. Thankfully all but one of those were revised and covered after having the doctor revise their notes.

If you’re in good health and value community sharing and low costs, Impact could be for you.

Other Health Sharing Ministries

While Impact Health Sharing has been a great fit for my family’s needs, there are quite a few other noteworthy alternatives in the health sharing ministries space that might appeal depending on your priorities.

For example, Medi-Share, with its 25-year track record of reliability and an unmatched 98% customer satisfaction rating, offers a strong, established community for sharing medical costs among Christian families, though it does require a statement of faith.

Zion HealthShare provides a more modern, non-denominational approach with straightforward guidelines and positive member feedback on handling serious conditions like cancer, ranking highly for its clarity and support.

Liberty HealthShare focuses on affordable sharing within a health-conscious community, but I’ve noted some concerning reviews about claim issues that could pose risks for the cautious among us.

Meanwhile, CrowdHealth stands out for its transparent comparisons to peers and emphasis on cost savings without religious requirements, making it a flexible choice for those prioritizing wellness incentives.

As someone who’s risk-averse, I’d advise comparing costs and coverage details carefully. When we signed up for a health sharing ministry we created a spreadsheet where we compared costs of all the different options. In our case Impact seemed to be the best fit.

Conclusion

Impact Health Sharing has been a game-changer for our family’s finances after one year. It’s affordable, efficient, and community-driven, though not without it’s hiccups like the pre-existing conditions clauses. If you’re exploring health insurance alternatives, give it a look. Here’s to healthier bodies and fatter portfolios!

FAQ

What is Impact Health Sharing?

Impact Health Sharing is a nonprofit health sharing ministry where members contribute monthly to share medical costs, offering an alternative to traditional insurance.

How does Impact Health Sharing differ from health insurance?

Unlike insurance, it’s not regulated as such and focuses on community sharing rather than profit. There’s no guarantee, but costs are lower, and it includes wellness perks.

What are the membership requirements for Impact Health Sharing?

Applicants must be 18+, commit to healthy living, and for seniors 65+, have Medicare Parts A and B. No religious requirement, though faith-inspired.

Can pre-existing conditions be covered under Impact Health Sharing?

It depends; they’re reviewed case-by-case, with no exclusions for seniors. Waiting periods may apply for some conditions.

How much can I save with Impact Health Sharing compared to insurance?

Members often save 30-50%, with plans starting at $73/month for individuals—potentially thousands yearly to redirect toward savings or investing. For a family like mine, we went from nearly $24,384 in potential annual out-of-pocket to about $10,036 plus co-share.

Is Impact Health Sharing suitable for families?

Yes, family plans start around $378/month, covering kids under 18, with flexibility for any provider. Our $628/month for a family of four has worked well.

What happens if a medical bill isn’t shared?

While rare, if ineligible, you’re responsible. Impact’s guidelines are clear, and their support helps navigate.

Impact Health Sharing

Pros

- Cost Savings

- Flexibility

- $0 Generic medications

- Wellness rewards

- Quick payouts to providers

Cons

- Not insurance

- Pre-existing conditions exclusions

- Not all providers will bill them

- Limitations on coverage

{kind=link}

Share Your Thoughts: