A few weeks ago I was looking at our health savings account (HSA) to figure out how much money we had left in the account.

We’ve had several large medical expenses lately, which we’ve already paid from our regular checking account. The expenses still need to be reimbursed from our HSA account once the funds are available.

While I was in the account to verify the available balance I began looking at the recent transactions in the ledger and I noticed that there was a charge on the HSA Visa card for something that was most certainly not a health related expense.

Uh oh.

The HSA account is meant to be used for health related expenses only, right? That’s why it receives favorable tax treatment.

What would this mean if we used the account to pay for something that wasn’t an health related expense? Would there be tax related penalties?

Quick Navigation

The Non-Health Related HSA Charge

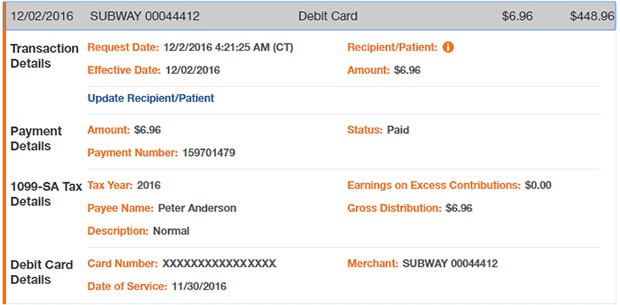

The charge that had gone through on our HSA card was $6.96 for a Subway sandwich shop near our house.

I went and talked with my wife about the transaction as I knew I hadn’t used the HSA Visa at a Subway recently.

When I talked with her she realized that she must have used it accidentally when paying for her food that day. The two Visa cards in her wallet, one for our checking and one for our HSA, look very similar. They both have the same color schemes, both are Visa cards, etc.

I was sure it wasn’t a big deal, but I knew I should research it more before doing our taxes.

What Is An HSA?

Health savings account (HSA) are pre-tax savings accounts that can be used to pay health care related expenses. They are used in conjunction with a high deductible health plan (HDHP), which is a health plan with a minimum deductible of $1300 for an individual, or $2600 for a family (in 2017). They also have to have a max out of pocket for costs of $6500 for an individual or $13,100 for a family.

| High Deductible Health Plan Requirements | 2019 | 2020 | 2021 |

|---|---|---|---|

| Minimum Annual Deductible Individual | $1,350 | $1,400 | $1,400 |

| Minimum Annual Deductible Family | $2,700 | $2,800 | $2,800 |

| Maximum Annual Out Of Pocket Individual | $6,750 | $6,900 | $7,000 |

| Maximum Annual Out Of Pocket Family | $13,500 | $13,800 | $14,000 |

Health savings accounts have been around since 2004, and the numbers of people using them have increased quite a bit over the last few years. As of January 2015 over 19.7 million people have an HSA in conjunction with a HDHP.

The HSA is a great way to save money on your taxes because you’re able to pay your health care expenses without having to pay taxes on the money first. The HSA account can be funded with up to $3400 for an individual, or $6750 for a family in 2017. (HSA Contribution Limits & Out of Pocket Costs)

| Health Savings Account (HSA) Contribution Limits | 2019 | 2020 | 2021 |

|---|---|---|---|

| Individual Limit | $3,500 | $3,550 | $3,600 |

| Family Limit | $7,000 | $7,100 | $7,200 |

So if you fully fund your account for your family this year that’s $6750 of income that is no longer taxable. That can save you a nice chunk of money – which is especially nice if you’re spending a decent amount on health care anyway.

Penalty For Non Medical Related HSA Distributions

So what happens when you spend HSA dollars on non medical expenses? In short, you’re going to have to pay a tax penalty on those particular distributions.

How do you determine if an expense is a health care related expense? The IRS defines what is and what isn’t an eligible expense in Publication 502.

In my case it’s pretty evident that our $6.96 charge at Subway is not health care related in any way. (We’re eating fresh? that’s good for your health, right?)

So what’s the penalty on our charge?

Tax Penalty

The tax penalty is 20% on any non-medical expenses before age 65. After you turn 65 you can use the HSA money for non health care related expenses without paying the penalty, but you will still have to pay income taxes on the money.

NOTE: There is a loophole where HSA distributions that are made by mistake can be reimbursed without penalty. It has to be because you truly believed something was covered as an eligible expense – when it wasn’t. In those cases where you thought something was in fact a covered medical expense you can reimburse the distribution without paying the penalty.

Reporting Your Erroneous HSA Charge

So what are you to do when you have an mistaken distribution like I did, and it’s clear it wasn’t a distribution because you thought it was a eligible medical expense?

At that point you just have to bite the bullet, claim the expense and pay your 20% penalty.

Reporting The Mistaken HSA Distribution

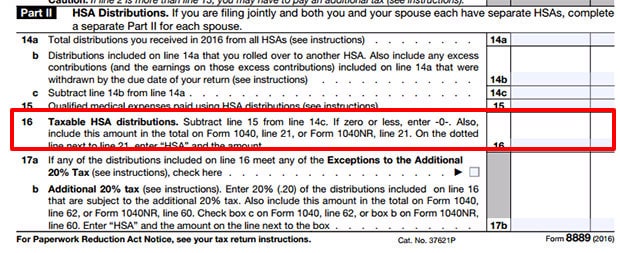

Just enter the amount of your ineligible distribution as a “Taxable HSA Distribution” on Line 16 of Form 8889 (Health Savings Accounts). Include this amount on Form 1040 as well on line 21, and enter “HSA” and the amount. In my case that would be $6.96.

Once you’ve done that calculate your additional 20% tax on line 17b of Form 8889, and then include that amount on your Form 1040, line 60. In our case that 20% penalty would be $1.39.

Once you’ve entered that information on your tax returns, you should be good to go.

Now you just have to make sure that next time you don’t give a nice 20% tip on your Subway sandwich to Uncle Sam. He doesn’t need it.

For more infomation on HSAs, see IRS Publication 969.

I agree with the content above and it is very factual, my only issue is that you probably would not have to pay the penalty in this situation. Ultimately at the end of the year it is a balancing act. How much was your qualified medical expense for the year and how much did you distribute from the HSA. As long as the HSA distributions did not exceed the qualified medical expenses for the year, you should be fine. It is like paying for the medical expense out of pocket and then taking money out of the HSA to reimburse yourself later.

I accidently had my tax refund deposited into my HSA. Is there anyone I can talk to about this??

really this in NO BIG DEAL! i wouldn’t even bother claiming it. one of the reasons i don’t use my HSA debit card is the fact that it is easier for the IRS to meddle into your business. so…i just reimburse myself every month. it’s rather easy for me. it can be all done online through electronic fund transfer directly into my personal checking account. again, don’t sweat it, and keep preppin’!

Where do you go to reimburse yourself?

I think the best approach to dealing with a problem like that is simply go back to the Subway, pay them $6.96 in cash and have them refund the transaction on the HSA card. If it’s too late for that, you could reimburse your HSA account with $6.96.

What do you do when you pay 2,400.00 for an eligible expense but for a child that is on the insurance but not eligible because we not longer claim him on our taxes?

Used my HSA as a personal checkings account and didn’t know. TD Bank reported in 2017 under my HSA that I made over ($25000) – how can i justify this to IRS. This was obviously a mistake. Rec’d a notice of deficiency from the IRS (They saying I owe $10000 in taxes and they hit me with a penalty) I only used my HSA contribution from my employer which was (1200) for only medical purposes and have proof but I need help in drafting a response.